Advanced (先端技術FPD搭載) TV市場~2024年は復活の年、2028年までに300億ドルに成長

出典調査レポート Quarterly Advanced TV Shipment and Forecast Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

Advanced (先端技術FPD搭載) TV市場~2024年は復活の年、2028年までに300億ドルに成長

- 2024年のAdvanced TVは、出荷数が前年比22%増、出荷額が15%増となる見通し。

- 2023-2028年のAdvanced TVの年平均成長率は、出荷数が10%増、出荷額が4%増となる見通し。

- 2024年通年では、MiniLED TVがOLED TVを出荷数、出荷額とも上回ると予測される。

Advanced TVは2023年に出荷数・出荷額とも減少したが、Q1'24には出荷数・出荷額とも回復が始まりQ2'24に加速、2024年は年間を通して好調を維持し2028年まで成長が続くと予測される。DSCCの Quarterly Advanced TV Shipment and Forecast Report 最新版が明らかにしている。

Advanced TV出荷数はQ2'24に前年比45%増となり、2024年通年では前年比22%増になると予測される。OLED TV出荷数はQ2'24に前年比2%増となり、2024年通年では前年比 4%増の見通しである。Advanced LCD TV出荷数はQ2'24に前年比53%増となり、2024年通年では前年比29%増になると予測される。2024年の成長をけん引するのは大画面製品で、77インチ以上のOLED TVの出荷数は14%増、75インチ以上のAdvanced LCD TVの出荷数は105%増になると見られる。

Advanced TV出荷額は2024年通年で前年比15%増になると予測される。OLED TV出荷額は前年比8%減、すべての画面サイズグループで前年比減となる見通しである。Advanced LCD TV出荷額は前年比29%増、75インチの出荷額は前年比22%増、75インチ以上の出荷額は前年比87%増になると見られる。

最新の長期予測では、2023-2028年のAdvanced TVの出荷総数は年平均成長率9%で増加すると予測される。OLED TV出荷数は2023年に16%減少したが、2023-2028年は年平均成長率9%で増加の見通しだ。Advanced LCD TV出荷数は2023年に前年比6%増加、2023-2028年は年平均成長率10%が見込まれている。2027年にはQD-OLEDを含むOLED TVがAdvanced TV出荷数全体の26%へとシェアを下げ、MicroLEDが非常に少ない台数ながら浮上してくるだろう。

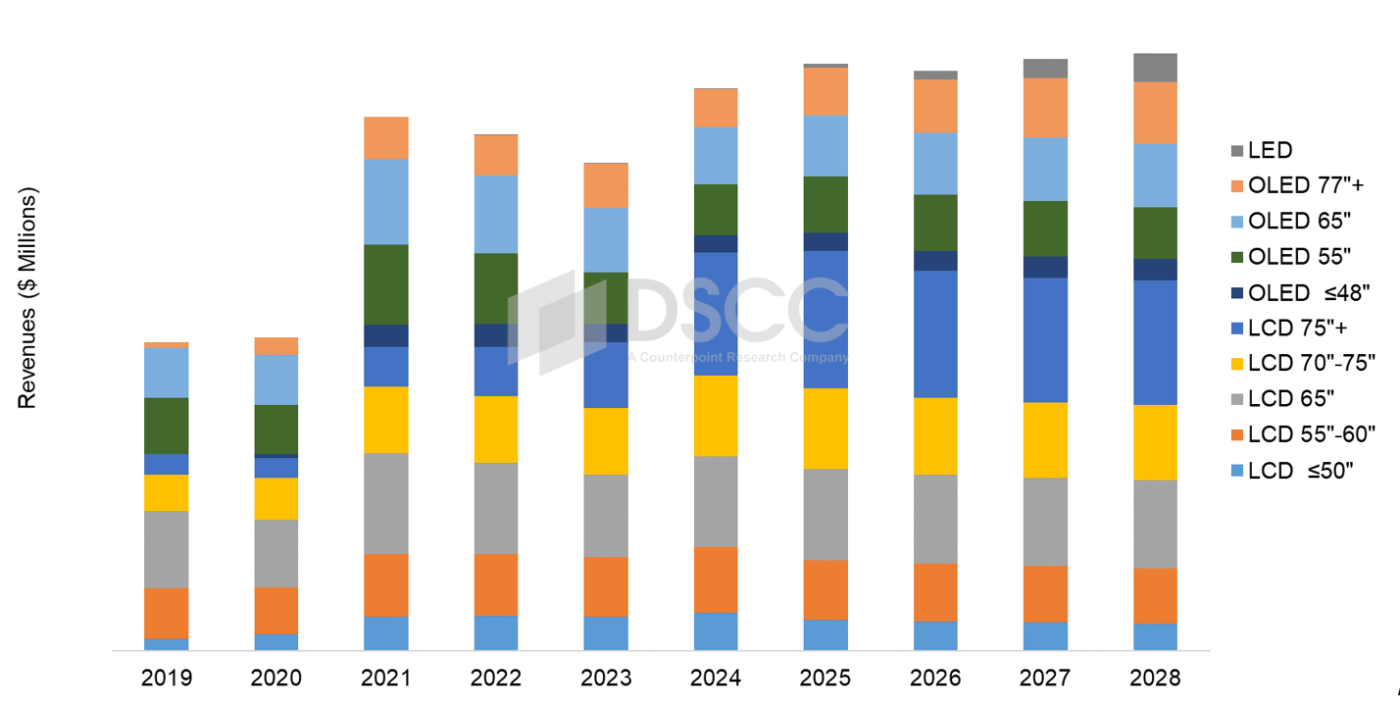

画面サイズ別および技術別Advanced TV出荷予測

Advanced TV出荷額は2021年にパンデミックによる需要と価格上昇で急増した。2022年には価格下落が数量増加を上回って出荷額は3%減少、2023年には軟調な需要を背景に価格下落が続き、出荷額はさらに5%減少した。2024年には出荷額が2021年のピークを上回り、前年比15%増になると予測される。成長は新たなピークである2028年の305億ドルまで続く見通しだ。

OLED TV出荷額は2023-2028年に年平均成長率2%で成長し101億ドルに達すると予測されるが、MiniLEDが大量に登場する前の2021年のピークを超えることはないだろう。Advanced LCD TV出荷額は年平均成長率4%で成長し2028年には189億ドルに達する見込みだが、2026-2028年は出荷額がほぼ横ばいになるだろう。

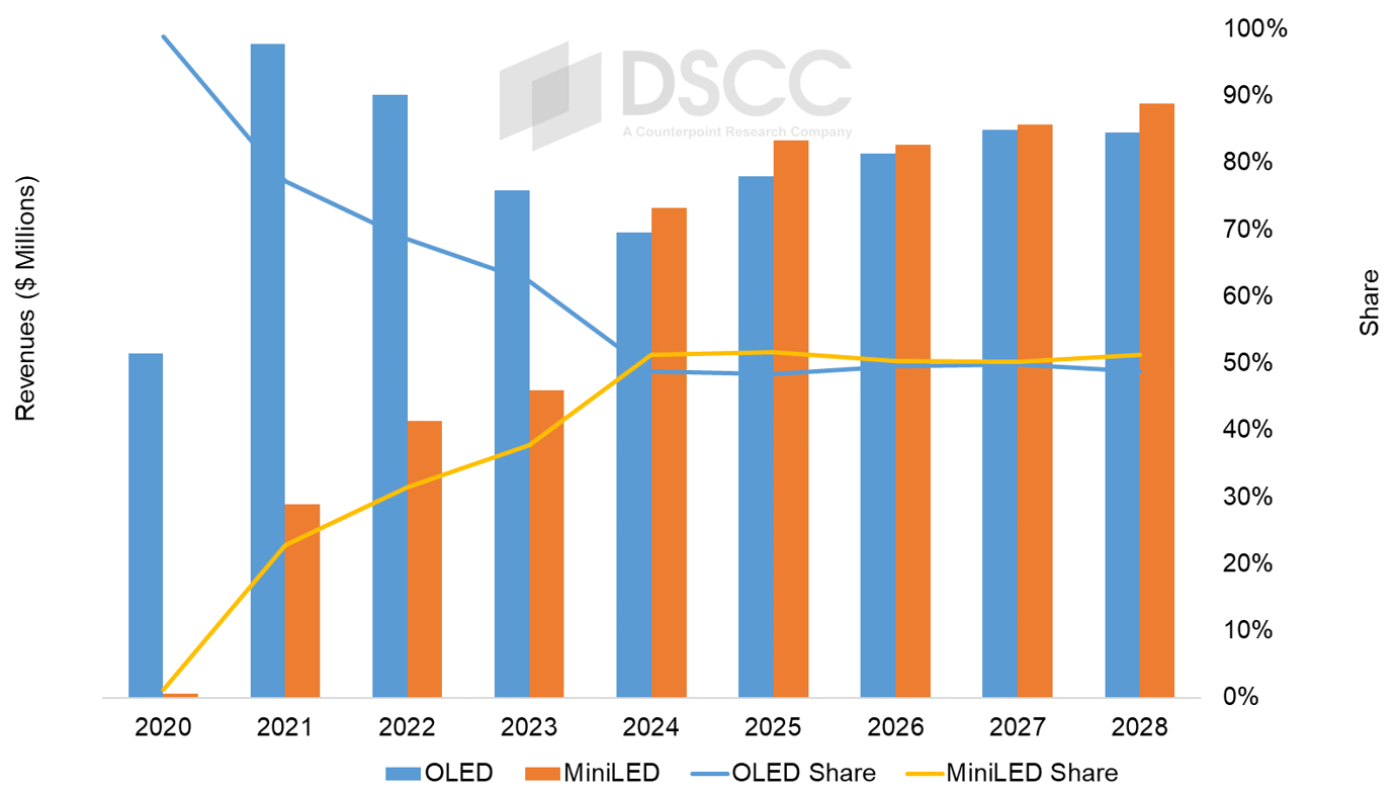

OLED vs. MiniLEDの戦いだが、MiniLEDは2021年から急成長したが2023年には出荷数および出荷額シェアでOLEDに遅れをとった。中国ブランドであるTCL、Hisense、Xiaomiの積極的な価格設定とプロモーションにけん引され、2024年にはMiniLEDが出荷数と出荷額ともにOLEDを上回り、超大画面のMiniLED TVはそれに比べて画面サイズが小さいOLED TVと同等の価格帯で十分に競争している。

MiniLEDは全サイズでLCDの費用対効果に強みがあるが、特に65インチ/75インチでは第10.5世代生産による優位性が高い。MiniLEDは75インチ以上のパネルではより低コストだが、OLEDはいずれの画面サイズでも最高価格とプレミアムブランドでトップクラスであることに変わりはない。「MiniLED + OLED」のプレミアムカテゴリーにおけるMiniLED TVのシェアは2023年に40%、Q2'24には54%に上昇しており、2024年通年では、MiniLED TVがOLED TVを出荷数、出荷額とも上回ると予測される。

OLEDはいずれの画面サイズでも最高価格とプレミアムブランドでトップクラスであることに変わりはないが、MiniLEDは大型サイズで優位であることから、MiniLEDの出荷額シェアは出荷数シェアと同等になる。OLED TV出荷額は2021年にピークを迎え2022-2023年に減少、2024年も減少が予測される一方、MiniLEDは成長している。「MiniLED + OLED」のプレミアムカテゴリーにおけるMiniLED TVの出荷額シェアは2023年に38%に上昇、2024年も51%まで引き続き上昇すると見られるが、その後は両技術のシェアが安定しそれぞれ約50%となり、MiniLEDがわずかに上回ると予測される。

画面サイズ別出荷額予測:OLED TV (左) ・MiniLED TV (右)

出典調査レポート Quarterly Advanced TV Shipment and Forecast Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] 2024 Will Be a Revival Year for Advanced TV Market with Growth to $30 Billion by 2028

- In 2024, Advanced TV units and revenues are expected to increase Y/Y by 22% and 15%, respectively.

- Advanced TV units and revenues are expected to increase by a 10% and 4% CAGR, respectively, from 2023-2028.

- MiniLED TVs are forecast to exceed OLED TVs in units and revenue for the full year 2024.

Advanced TV shipments declined in both units and revenue in 2023, but a recovery in both units and revenue started in Q1 2024, accelerated in Q2 and will continue strong through the full year 2024, and we expect growth to continue to 2028, according to the latest update to DSCC’s Quarterly Advanced TV Shipment and Forecast Report, now available to subscribers.

Total Advanced TV shipments increased 45% Y/Y in Q2’24 and we forecast an increase of 22% Y/Y for the full year 2024. OLED TV units increased 2% Y/Y in Q2’24 and we forecast a 4% increase Y/Y for the full year 2024. Advanced LCD TV units increased 53% Y/Y in Q2’24 and we forecast growth of 29% for the full year 2024. Large screens will drive the growth in 2024, as 77”+ OLED TV shipments are forecast to increase by 14%, and >75” Advanced LCD TV shipments are forecast to increase by 105%.

For the full year 2024, we forecast Advanced TV revenues to increase by 15% Y/Y. OLED TV revenues are forecast to decline by 8% Y/Y, with all screen size groups forecast to have revenues decrease Y/Y. Advanced LCD TV revenues are forecast to increase by 29% Y/Y, with 75” revenues to increase Y/Y by 22%, and >75” revenues to increase by 87% Y/Y.

In our updated long-term forecast, total Advanced TV shipments are expected to grow by an 9% CAGR from 2023 to 2028. We estimate that OLED TV units declined 16% in 2023, but we expect them to grow at a 9% CAGR from 2023-2028. We estimate that Advanced LCD TV units increased by 6% Y/Y in 2023 and we expect them to grow at a 10% CAGR from 2023-2028. Including QD-OLED, OLED TV will be reduced to a 26% share of Advanced TV units in 2027, and MicroLED will emerge with very small volumes.

Advanced TV revenues jumped in 2021 with pandemic-fed demand and higher prices. Revenues declined in 2022 by 3% as price declines overwhelmed volume increases and declined another 5% in 2023 as prices continued to decline with soft demand. We expect revenues to surpass the 2021 peak in 2024 and increase by 15% Y/Y. Growth will continue to a new peak in 2028 of $30.5 billion.

OLED TV revenues are expected to grow at a 2% CAGR from 2023 to 2028 to $10.1B but will not exceed the revenue peak in 2021 which happened before MiniLED came on the scene in high volumes. Advanced LCD TV revenues are expected to grow at a 4% CAGR to $18.9B in 2028, but revenues are close to flat for 2026-2028.

In the OLED vs. MiniLED battle, MiniLED has grown rapidly from 2021 but remained behind OLED in unit and revenue share in 2023. Driven by aggressive pricing and promotion from Chinese brands TCL, Hisense and Xiaomi, MiniLED has surpassed OLED in both units and revenues in 2024, with ultra-large screen MiniLED TVs competing well at price points equal to smaller screen OLED TVs.

MiniLED has an advantage in LCD cost-effectiveness across all sizes but especially in 65”/75” because of Gen 10.5 production, and MiniLED has lower costs for >75” panels, but OLED remains the top tier at each screen size with the highest prices and the premium brands. MiniLED TV share of the premium “MiniLED + OLED” category increased to 40% in 2023 and 54% in Q2’24, and we expect that MiniLED will surpass OLED in both units and revenue for the full year 2024.

Although OLED remains the top tier at each screen size with the highest prices and the premium brands, MiniLED’s advantage in large sizes allows its revenue share to match unit share. OLED TV revenue peaked in 2021 and declined in 2022-2023 and is expected to decline again in 2024 while MiniLED has grown. MiniLED TV revenue share of the premium “MiniLED + OLED” category increased to 38% in 2023 and we expect MiniLED TV revenue share of the premium space will continue to increase to 51% in 2024, and then for the two technologies to stabilize their share, each at about 50% with MiniLED having a slight advantage.