AppleのOLED iPad Proは最高品質ディスプレイ搭載の最薄タブレット、しかしパネル出荷数は右肩下がり

[出典] 講演資料集を販売中!

Display 360 Summit の講演資料集には、スマートフォン/TV/車載/IT市場の需要に関するDSCCの最新見解とディスプレイ製造/設備投資/MicroLEDに関するDSCCの予測のほか、Amorphox、Coherent、Counterpoint Research、Intel、Kateeva、Intel、Lumileds、Nanosys、Saphluxのプレゼンテーションを収録しています。Display 360 Summitの講演資料集については、セミナー専用サイト にアクセスいただくか、info@displaysupplychain.com までお問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

AppleのOLED iPad Proは最高品質ディスプレイ搭載の最薄タブレット、しかしパネル出荷数は右肩下がり

DSCC主催セミナー (米国10月2日) の Display 360 Summit で明らかになったように、Appleの第1世代OLED iPad Pro用パネルの需要が、好調だった第2四半期を経て、鈍化している。タンデムOLEDスタック/LTPSバックプレーン/厚さ0.2 mmという、タブレット市場向けにこれまで製造されたなかでおそらく最高のディスプレイが市場最薄のタブレットに収められているのだが。。。

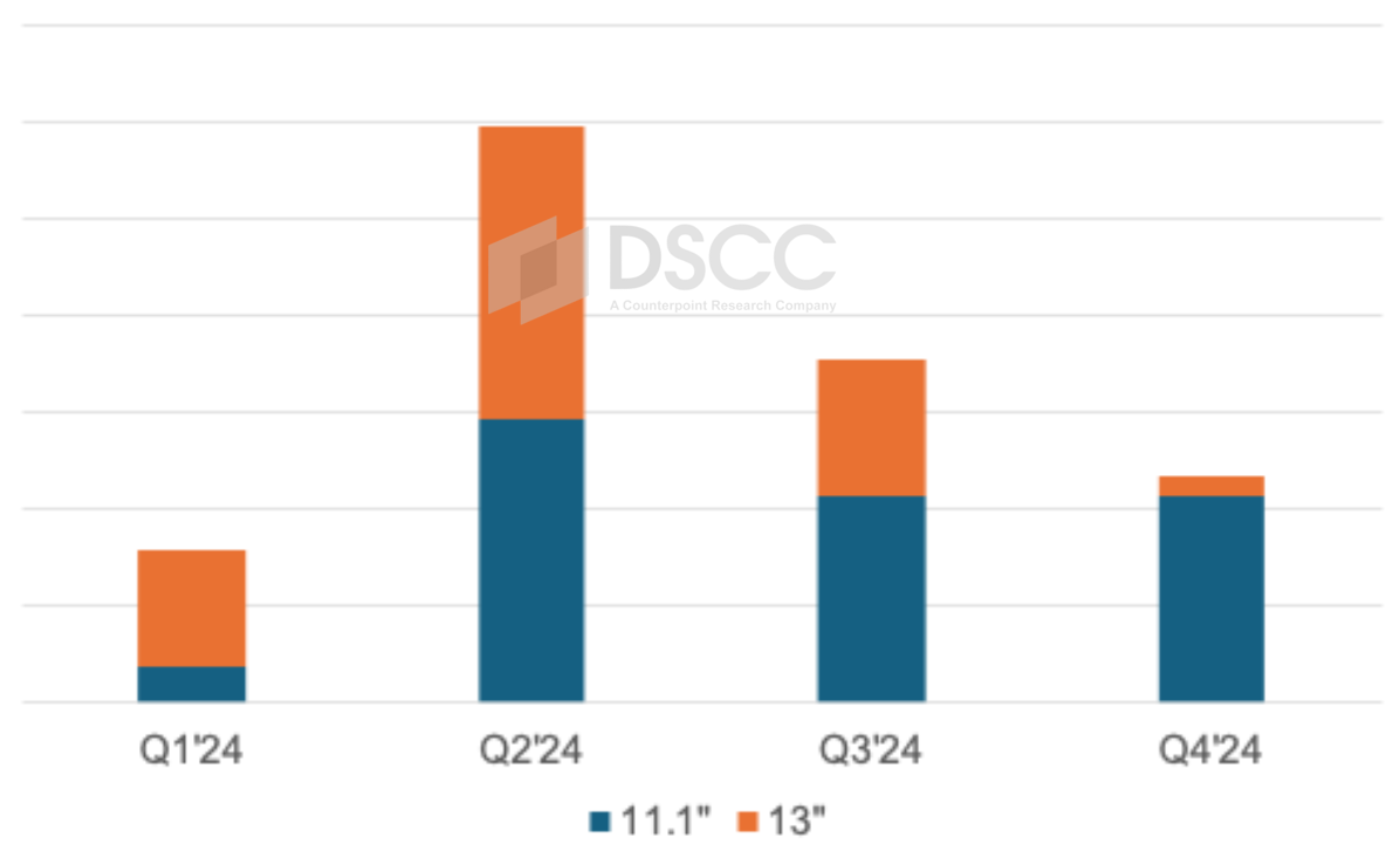

優れたディスプレイと魅力的なフォームファクターにもかかわらず、2024年の11.1インチおよび13インチiPad Pro用パネル出荷数は当初の予測を大幅に下回る見通しとなっている。当初の予測は1000万枚と高かったが、現在はわずか670万枚の見込みで、ディスプレイサイズ別では以下のグラフの通りである。Q3’24のiPad Pro用OLED出荷数は暫定値で40%減となっており、Q4’24は30%以上の減少が見込まれている。高価格の13インチモデルで以下の通り最も大きな減少が見られ、Q3’24は50%以上減少、Q4’24には90%以上の減少が予測される。製品発表に向けてQ2’24に大量のパネルを出荷しアーリーアダプターの需要に対応した後、需要は完全に枯渇したようだ。

サイズ別 iPad Pro用OLED出荷数

OLED iPad Proに一体何が起こっているのだろうか。

- 第一に、11.1インチが999ドル、13インチが1299ドルという高価格であること。スマートフォンやノートPCを補完する役割が一般的である製品としては高すぎる価格だ。

- 第二に、タブレットは長持ちする。高速M4プロセッサや優れたディスプレイは、消費者が食品や住宅、エネルギーの価格高騰に苦しんでいる現状では特に、人々に買い替え期間を短縮させるには十分ではない。AppleはおそらくiPadの下取り価格を引き上げる必要があるだろう。

- 第三に、ディスプレイやフォームファクターは確かに素晴らしいが、ほとんどの人々にとってはそれほど目立った差ではない。高価格をともなうiPadOSの限界で需要は抑え気味で、必需品というより「あったらいいな」という製品である可能性が高い。そのため、OLED搭載による価格プレミアムが当然のものとして受け入れられ、なおかつ大量販売が可能なのか、という疑問が生まれる。OLEDはAdvanced (先端技術FPD搭載) TV市場でMiniLEDに主導権を奪われており、OLED TVの価格は通常、20インチ大きいLCDと同じ程度であるため、大幅な価格差を克服できていない。M2プロセッサを搭載したiPad Proの最終世代モデルにはMiniLEDが採用された。M4チップとOLEDへの切り替えは、多額の支出に見合うだけの性能や体験の違いを生み出していない可能性が高い。

- 超薄型iPadの需要が予想を下回っていることは、来年発売予定の超薄型iPhoneにとって悪いニュースなのだろうか。

さて、これはAppleとIT用OLED生産ラインにとって何を意味するのだろうか。 FPDメーカーはOLED iPad Proの需要の低迷が他のApple IT製品、特に他のiPadの需要にも影響を与えるのではないかと不安視している。そのため、AppleがiPad AirモデルのLCDからOLEDへの切り替えを1年以上遅らせる可能性が懸念されている。この傾向が続けば、IT用OLEDに対する需要が高まるまではIT用OLED生産ラインへの数十億ドル規模の投資を控えるFPDメーカーも出てくるかもしれない。

ただし、iPadでいま起こっている事態と似たようなことが今後MacBookでも必ず起こるとは考えていない。OLEDタブレットよりもOLED MacBookに対する潜在需要の方が強いと考えており、また、PCブランド各社は引き続きOLED搭載モデル数を増やしているとも聞いている。ということで、IT用OLED生産ラインの大幅な延期はないかもしれない。現時点では新たな延期情報は確認されていない。

------------------------------------

Display 360 Summit の講演資料集には、スマートフォン/TV/車載/IT市場の需要に関するDSCCの最新見解とディスプレイ製造/設備投資/MicroLEDに関するDSCCの予測のほか、Amorphox、Coherent、Counterpoint Research、Intel、Kateeva、Intel、Lumileds、Nanosys、Saphluxのプレゼンテーションを収録しています。Display 360 Summitの講演資料集については、セミナー専用サイト にアクセスいただくか、info@displaysupplychain.com までお問い合わせください。

[原文] Apple’s OLED iPad Pro Volumes Continue to Come Down Despite Having the Tablet Market’s Best Display and Thinnest Form Factor

As revealed at our Display 360 Summit, Apple’s first generation OLED iPad Pro panel demand has really slowed down after a strong Q2’24 despite arguably having the best displays ever produced for the tablet market with tandem OLED stacks, LTPS backplanes, 0.2mm thickness and packaged in the thinnest tablets on the market.

Despite superior displays and an attractive form factor, 2024 panel shipments for the 11.1” and 13” iPad Pro’s are expected to fall way short of initial expectations. While initial expectations were as high as 10 million (M), we now see just 6.7M as shown below by display size. Preliminary Q3’24 figures show a 40% decline in OLED iPad Pro panel shipments and Q4’24 is expected to be down over 30%. The higher priced 13” models are seeing the largest reductions as shown below, down over 50% in Q3’24 and are expected to be down 90% or more in Q4’24. It appears that after satisfying the early adopter demand with a large number of panels shipped in Q2’24 for the product launch, demand has really dried up.

What is going on with the OLED iPad Pro’s?

- First, the high prices which start at $999 at 11.1” and $1299 at 13”. That is a high price to pay for a product that is typically complementary to a smartphone or a laptop.

- Second, tablets last a long time. The faster M4 processor and better displays aren’t causing enough people to shorten their replacement periods, especially when consumers are still struggling with high food, housing and energy prices. Perhaps Apple needs to boost their iPad trade-in values.

- Third, although the displays and form factor are truly impressive, it is just not moving the needle for most people. It is likely a “nice to have” product rather than a necessity given the limitations of the iPadOS which along with the high price is limiting demand. This begs the question of whether OLEDs can command a premium and still drive high volumes. OLEDs have lost leadership in Advanced TVs to MiniLEDs, not able to overcome the substantial price difference with OLED TVs typically priced similar to LCDs 20” larger. The last generation of iPad Pro’s with M2 processors used MiniLEDs. The switch to M4 chips and OLEDs is likely not creating enough of a performance or experience difference to justify the large spend.

- Does the weaker than expected demand for the ultra-thin iPads spell bad news for the ultra-slim iPhone expected next year?

So what does this mean for Apple and IT OLED fabs? Well, panel suppliers are concerned that the tepid demand for OLED iPad Pro’s will also impact demand for other Apple IT products, especially other iPads. For this reason, there are concerns that Apple could delay the switch of iPad Air models from LCD to OLED by a year or longer. If this trend continues, this may cause some panel suppliers to wait longer to see stronger IT OLED demand before spending billions on an IT OLED fab.

However, we don’t believe what is happening in iPads will necessarily be analogous to what could happen in MacBooks. We believe there is stronger pent-up demand for OLED MacBooks than tablets and also hear that PC brands continue to increase the number of models with OLEDs. So, perhaps we won’t see any major delays in IT OLED fabs. We haven’t seen any new delays at this point.

For access to the Display 360 proceedings which include DSCC’s latest insights into smartphone, TV, automotive and IT market demand as well as DSCC’s outlook for display manufacturing, equipment spending and MicroLEDs along with presentations from Amorphyx, Coherent, Counterpoint Research, Intel, Kateeva, Intel, Lumileds, Nanosys and Saphlux, please visit https://www.accelevents.com/e/... or contact info@displaysupplychain.com.