AppleのOLED iPad Proのサイズ構成に変化

関連調査レポート Quarterly Advanced IT Display Shipment and Technology Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEBご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

AppleのOLED iPad Proのサイズ構成に変化

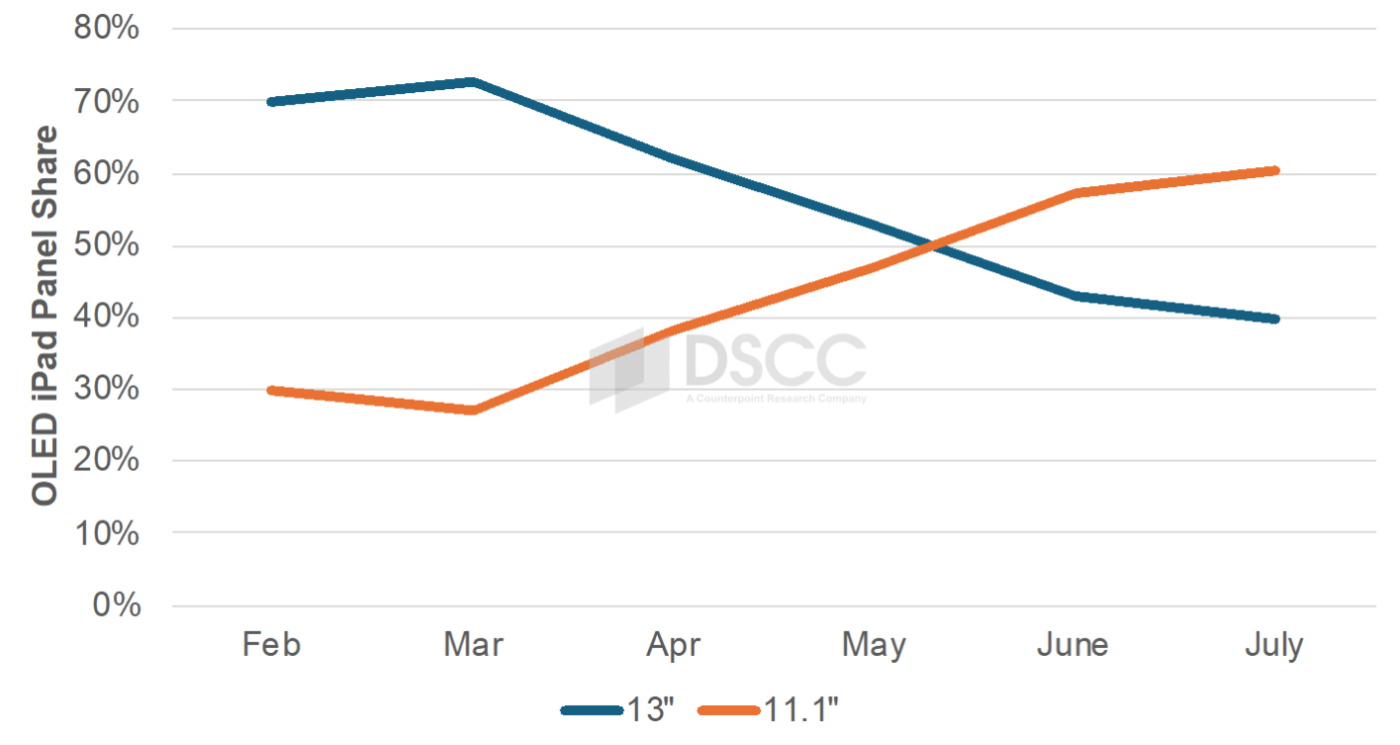

AppleのiPad Pro用OLED調達について、DSCCではサプライチェーン情報筋を通じて月次ベースで追跡を続けている。2月から3月の生産開始当初にそのデータを見て、11.1インチと13インチの配分が大きく13インチに傾いており、70%以上のシェアを占めていることに驚かされた。価格が300ドル安いことから、11.1インチが13インチより多く売れる可能性があると考えていたためだ。私たちがそのように考えていた根拠は、SDCがタンデムスタックにおけるクロストーク/光漏れの対処について技術的課題を抱えていた可能性があること、そしてSDCが11.1インチで支配力を持つサプライヤーだったことである。一方で13インチ支持意見の論拠は、出荷数の大半は大型サイズ需要が高い米国と欧州で発生する、というものだった。4月と5月の動きを見ると、13インチと11.1インチの差がかなり縮まっており、11.1インチのシェアは4月には約40%、5月には約50%に達している。SDCが技術的課題を解決した可能性があり、それと同時にLGDがセカンドサプライヤーとして加わったことで出荷数が増え始めたようだ。

AppleのiPad Pro用OLED調達 サイズ別シェア

6月と7月に目を向けると、11.1インチがシェアを伸ばす傾向が続いており、6月はほぼ60%、7月はちょうど60%になると予測される。LGDの11.1インチシェアは5月までは1桁だったが、7月は20%を超える見通しだ。iPad Pro用OLED調達数は5月から月100万枚を超えており、少なくとも7月までは続くと見られる。調達ベースではQ2'24が今年のピークとなる可能性が高く、Q3’24は若干減少、Q4’24はさらに減少すると予測される。

LGDとSDCの間のシェア推移については、パネルサイズのトレンドに似ている。LGDが2月と3月にシェア70%以上でスタートしたが、4月には60%台後半、5月には50%台後半で、両社の差が縮小している。6月と7月は50:50にかなり近くなると見られる。

関連調査レポート Quarterly Advanced IT Display Shipment and Technology Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEBご試読は こちらから お問い合わせください。

[原文] Apple’s OLED iPad Pro’s Undergo a Mix Shift

We continue to track Apple’s OLED iPad Pro panel procurement on a monthly basis through our supply chain contacts. Looking at the data, we were initially surprised when production started in February and March that the allocation between 11.1” and 13” heavily favored 13” with at least a 70% share. Given the $300 lower price, we thought that 11.1" might outsell 13". Our understanding for this was that SDC may have had some technical challenges managing crosstalk/light leakage in the tandem stack and SDC was the dominant 11.1” supplier. The argument for 13" was that most of the volume would occur in the US and Europe where larger sizes are in higher demand. Looking at April and May, we saw that the gap closed quite a bit between 13” and 11.1” with 11.1” reaching nearly a 40% share in April and nearly a 50% share in May. It appears that SDC may have solved their technical challenges and, at the same time, LGD was added as a second supplier and started shipping higher volumes.

Looking at June and July, the trend for 11.1” to gain share is continuing with 11.1” expected to account for nearly a 60% share in June and exactly a 60% share in July. LGD’s share at 11.1” was single digits through May but is expected to exceed 20% in July. OLED iPad Pro panel procurement volumes have exceeded 1M per month from May and that is expected to continue through at least July. We expect Q2’24 to likely be the peak quarter for the year on a procurement basis with only a small drop in Q3’24 and a larger drop in Q4’24.

In terms of LGD vs. SDC share, the trend is similar to the panel size trend. LGD started out with a 70%+ share in February and March, it narrowed to high 60s in April and high 50s in May. In June and July, it is expected to be quite close to 50/50.

For more insight into the OLED tablet market, please see our Quarterly Advanced IT Display Shipment and Technology Report.