TV用LCD価格月報~国慶節休暇の操業停止で価格下落が減速

出典調査レポート Quarterly All Display Fab Utilization Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

TV用LCD価格月報~国慶節休暇の操業停止で価格下落が減速

中国の主要LCDメーカー各社による国慶節休暇の操業停止により第4四半期に向けて業界の供給量が減少した結果、TV用LCD価格が持ち直している。LCD価格は第4四半期に入っても下落しているが、そのペースは鈍化している。価格上昇につながる需要のけん引役は見当たらないものの、価格下落のペースはかなり緩やかで横ばいに近い状態だ。

Q2’24の稼働率上昇と需要低迷によって今年春の価格上昇に終止符が打たれた。DSCCの Quarterly All Display Fab Utilization Report によると、LCDメーカーの稼働率はQ1’24の77%からQ2'24には86%に上昇した。LCD TFT総投入量はQ4'23からQ1'24の減速を経てQ2'24には前期比12%増となった。稼働率はQ3’24にやや低下したと推測されるが、10月初旬の操業停止を織り込んだ当初予測を上回る結果となった。

中国FPDメーカー各社は国慶節休暇に合わせ10月初旬に生産ラインを停止しているが、これは業界の供給コントロールに向けた異例の措置だ。例年、国慶節休暇の停止は1-2日間だけだが、今年は1-2週間になることを各社が示唆している。

需要面に目を向けると、TV需要は依然低調で、Q2’24のTV出荷総数は前年比3%増だったことをCounterpoint Researchの Quarterly Global TV Shipments Tracker が明らかにしている。欧州のスポーツイベントを見越したTVパネル需要の盛り上がりが前年比成長の要因となったが、第3四半期については、数値データによる裏付けはないものの初期の動向を見る限り、比較的低調な四半期になりそうだ。

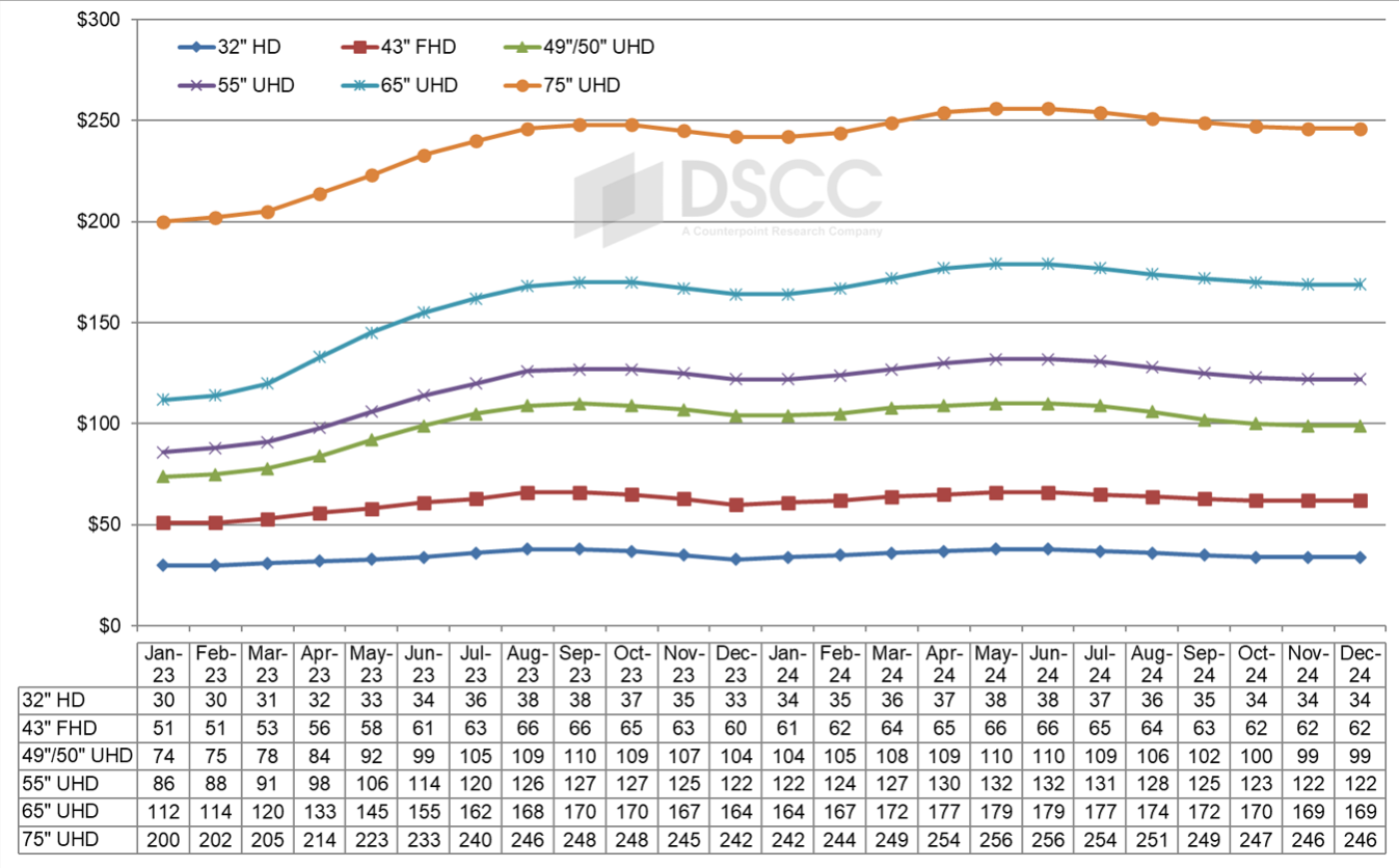

一つ目のグラフは2024年12月までのTV用LCD価格動向の最新予測である。価格は2022年9月に過去最低値を記録した後、パンデミック後の最初の反発局面が始まった。価格はQ2’23とQ3’23に上昇した後、Q4’23にはやや低迷、Q1’24からQ2’24にかけて緩やかに上昇した。9月の価格は当初予測と同等またはわずかに低い水準となり、これを受けて10月の価格予測は先月と比べやや高くなっている。

TV 用LCD価格

Q2’24の価格は前期比で平均5.5%高と大きく上昇した。価格は7月に下がり始め、第3四半期は平均2.8%の下落となった (先月予測では3.0%下落の見込みだった) が、第3四半期の平均価格は第1四半期よりも高い水準を維持するだろう。Q4’24の価格は前期比4.0%下落と予測される。

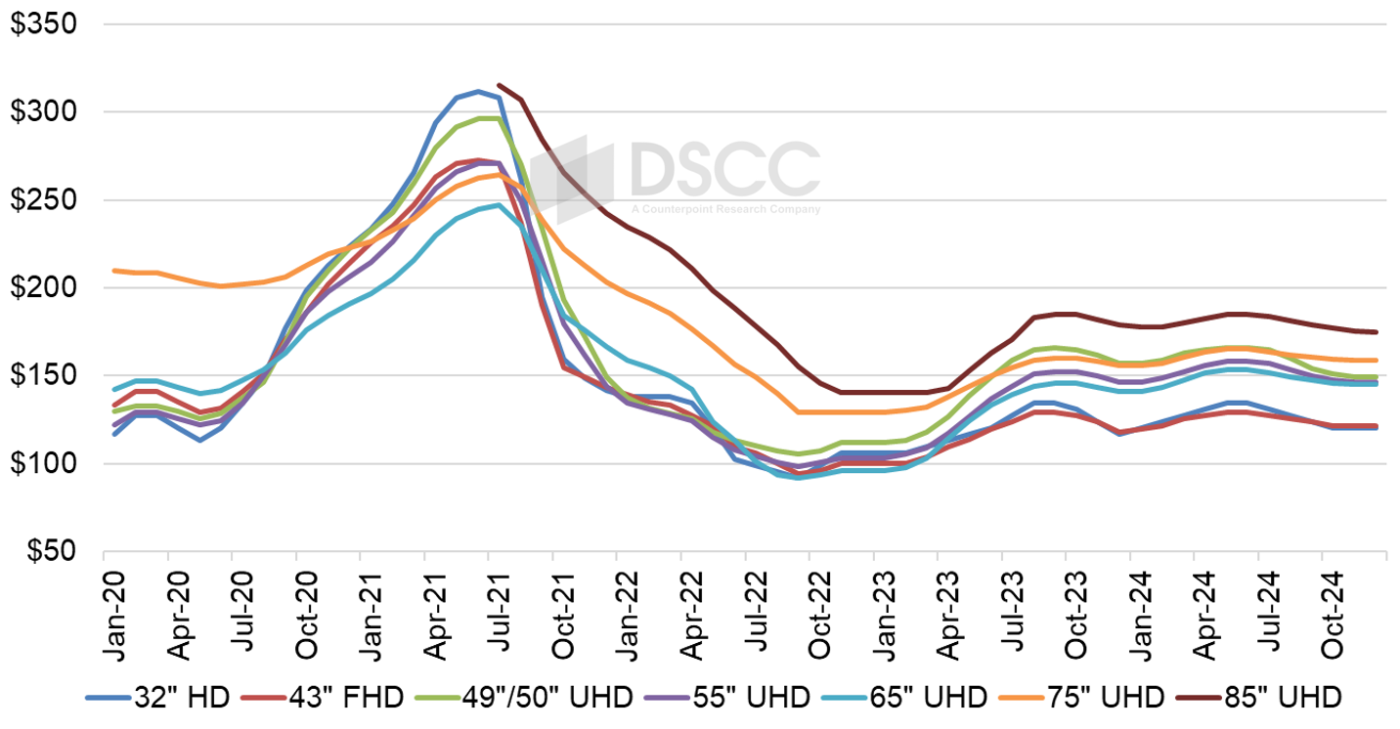

面積ベースの価格を見ると、供給過剰の典型的なパターンが見られる。当社のインデックスで最も小さいTV用パネルサイズである32インチは、業界の価格設定における「炭鉱のカナリア」だ。32インチパネルの価格は、供給制約のときに最初に上昇し、供給過剰のときには最初に下落する。このパターンは2024年上半期の上昇局面で実証され、2024年下半期の下落局面でも示されている。

前回最安値を示した2023年12月のパネル面積価格 (1平方メートルあたり) は、32インチが117ドル、43インチが118ドルでそれぞれ最低水準だったが、65インチ (141ドル) 、55インチ (146ドル) 、75インチ (156ドル) 、49インチ/50インチ (157ドル) のパネル面積価格はそれよりも高かった。32インチに対する65インチのパネル面積価格プレミアムは12月には21%だったが、6月には14%に下がった。現在は市場が供給過剰に転じたためプレミアムは上昇しており、10月には21%に達すると予測される。

49インチ/50インチは今年中盤の上昇サイクルで特に価格が上昇したが、43インチパネルの面積価格は業界最低水準だった。43インチに対する49インチ/50インチのプレミアムは1月の31%からやや下がったが4月から8月までは28-29%で安定、9月には25%まで下がった。第4四半期には49インチ/50インチ価格が43インチ価格よりもやや速いペースで下落し、プレミアムは23%まで下がると予測される。43インチに対する49インチ/50インチの価格プレミアムは第8.5世代の生産能力を持つLCDメーカーに有利に働き、その代償を負うのは第10.5世代のLCDメーカーだ。第10.5世代生産ラインでは43インチを18面取りで非常に効率的に生産できるが、49インチ/50インチの面取り効率は良くない。一方、第8.5世代生産ラインでは49インチ/50インチパネルを8面取りで効率的に生産できる。

TV用LCD面積価格 (1平方メートルあたり)

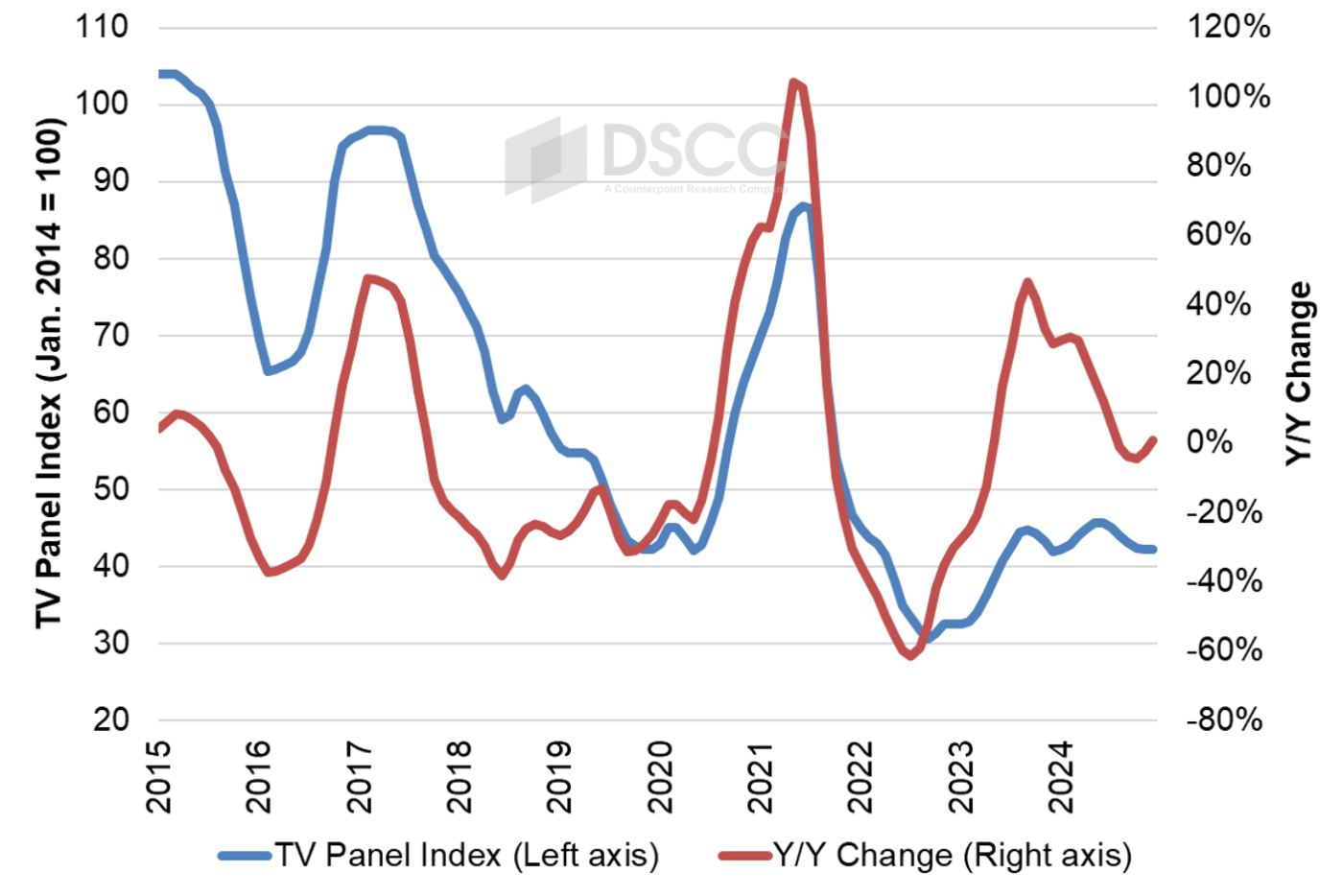

最後のグラフは2015年から2024年12月までの長期的視点によるTV用LCD価格指数を示している。2023年の価格上昇によってDSCCの指数は2023年9月に44.8に到達、2022年9月の30.5という最低値と比べ47%上昇した。2023年12月には指数が41.8まで下落、直近のピークから7%下がったものの、前年比では29%上昇、過去最低値と比較すると37%上昇となった。2024年5-6月には再びピークの45.6に達した。これは昨年のピークをわずかに上回っており、2022年9月の過去最低値と比べ49%上昇となった。今後は2024年11月に42.1まで下落し12月は横ばい、1年前の最低値をやや上回る水準となる見通しだ。

TV用LCD価格指数

このグラフにはパネル価格の最近のパターンにおけるもう一つの興味深い特徴が示されている。2024年9月時点で価格指数は15ヵ月間、41.8から45.6の比較的狭い範囲内、10%未満の範囲に留まっている。これは少なくとも2015年以降は見られなかったTV用LCD価格の安定期間を表しており、少なくとも12月まではこの範囲内に留まることが予測される。

TV用LCD価格の上昇によってLCDメーカーの収益性はQ2’24に改善し、大型LCDに重点的に取り組んでいる中国のLCDメーカー3社、すなわちBOE、CSOT、CHOTのいずれも第2四半期に利益を計上した。第3四半期の稼働率が予想を上回ったことでTV用LCD価格には多少の下げ圧力がかかったが、中国のLCDメーカーは操業停止によって供給量を抑制する意向を示した。これにより、価格は安定しつつあるようだ。

出典調査レポート Quarterly All Display Fab Utilization Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] China National Day Shutdown Slows Down LCD TV Panel Price Declines

A shutdown by major Chinese LCD makers for the country’s National Day holiday has reduced industry supply leading into the fourth quarter, and as a result has firmed up LCD TV panel prices. While panel prices are still coming down in Q4, the pace of decline has slowed. While we do not see any demand drivers that could push prices up, the pace of price declines is very gradual, approaching flat.

Higher utilizations in Q2’24 combined with soft demand to bring this year’s springtime rally to an end. Based on DSCC’s Quarterly All Display Fab Utilization Report, LCD makers increased their utilization from 77% in Q1’24 to 86% in Q2’24. After a slow Q4’23 and Q1’24, total LCD TFT increased by 12% Q/Q in Q2’24. We estimate that utilization slowed down slightly in Q3’24 but ran higher than our initial expectation in the third quarter in anticipation of a shutdown in early October.

Chinese panel makers have shut down their fabs in early October for the National Day holiday, an unusual step to control industry supply. Normally, the National Day shutdown may be only one to two days, but this year panel makers indicate it will be one to two weeks.

On the demand side, TV demand has remained tepid, with overall TV shipments increasing 3% Y/Y in Q2’24, according to the Counterpoint Research's Quarterly Global TV Shipments Tracker. The boost in demand for TV panels in anticipation of European sporting events spurred the Y/Y increase, but the early anecdotal evidence about Q3 suggests a relatively weak quarter.

The first chart here highlights our latest TV panel price update with a forecast to December 2024, starting with the first post-pandemic rally, which started after prices hit their all-time lows in September 2022. Prices increased in the middle of two quarters of 2023, followed by a mild slump in Q4’23 and a mild rally in Q1-Q2’24. Prices for September came in equal to or slightly higher than our expectations, and as a result our forecast for October prices are slightly higher compared to last month.

Prices in Q2’24 saw a robust average price increase of 5.5% Q/Q. With prices falling starting in July, we saw an average price decrease in Q3 of 2.8% (last month we estimated this at 3.0%), but the average Q3 prices will remain higher than the Q1 average. We now expect a 4.0% price decrease in Q4’24 compared with Q3.

As we look at pricing on an area basis, we are seeing a pattern characteristic of oversupply. The smallest TV panel size in our index, 32”, is the ‘canary in the coal mine’ of pricing in the industry. The prices for 32” panels are the first to go up with a supply constraint and are the first to go down in an oversupply. We have seen that pattern bear out in the rally in the first half of 2024 and we are seeing it in the slump in the second half of 2024.

At the prior low point in December 2023, 32” and 43” panels had the lowest area price at $117 and $118 per square meter, respectively, but area prices were higher for 65” ($141), 55” ($146), 75” ($156) and 49/50” ($157). The area price premium for 65” panels over 32” panels was 21% in December, but it was reduced to 14% in June. Now as the market has shifted to oversupply, we are seeing that premium increase and expect it to reach 21% in October.

The area prices for 49”/50” were especially strong in the mid-year up-cycle, while area prices for 43” panels were the lowest in the industry. The premium for 49”/50” over 43” started the year at 31% in January and declined slightly but stabilized at 28-29% from April through August before declining to 25% in September. We expect that 49”/50” prices will decline slightly faster than 43” prices in the fourth quarter and the premium to drop to 23%. A premium for 49”/50” over 43” favors panel makers with Gen 8.5 capacity at the expense of those with Gen 10.5 capacity. Gen 10.5 fabs can make 43” very efficiently with an 18-up configuration, but do not have an efficient cut for 49”/50”, while Gen 8.5 fabs can make 49”/50” panels efficiently with an 8-up configuration.

Our final chart in this sequence shows our LCD TV panel price index, taking a longer view from 2015 through December 2024. The price increases in 2023 brought our index up to a peak of 44.8 in September 2023, an increase of 47% compared to the low of 30.5 in September 2022. The index declined to 41.8 in December 2023, which was down 7% from the recent peak but still up 29% Y/Y and up 37% compared to the all-time low. Prices peaked again in May/June 2024 at 45.6, slightly higher than last year’s peak and 49% higher than the all-time low of September 2022. We now expect prices to fall to 42.1 in November 2024 and to stay there in December, slightly higher than the low point a year ago.

The chart reveals another intriguing characteristic of the recent pattern in panel prices. As of September 2024, prices have remained for fifteen months within a relatively tight range between 41.8 and 45.6, less than a 10% range. This represents a period of stability in LCD TV panel prices not seen since at least 2015, and we expect that prices will remain within this range at least through December.

The higher LCD TV panel prices helped panel makers to improved profitability in the second quarter of 2024, as the three Chinese panel makers focused on large-screen LCDs – BOE, CSOT and CHOT – all reported profits in Q2. The higher-than-expected utilizations in the third quarter put some downward pressure on LCD TV panel prices, but the Chinese panel makers have signaled with their shutdown that they intend to keep supply under control. That seems to be stabilizing prices.