FPD製造装置市場は2024年に回復へ

出典調査レポート Quarterly Display Capex and Equipment Market Share Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

冒頭部和訳

- FPD設備投資は、2023年に59%減少となった後、2024年には54%増と大きく成長する。

- 2024年はSamsung DisplayのA6 fabがシェア30%で設備投資額トップとなる。

- Canon/Tokkiが100%超の成長、シェア13%の製造装置メーカー首位となる。

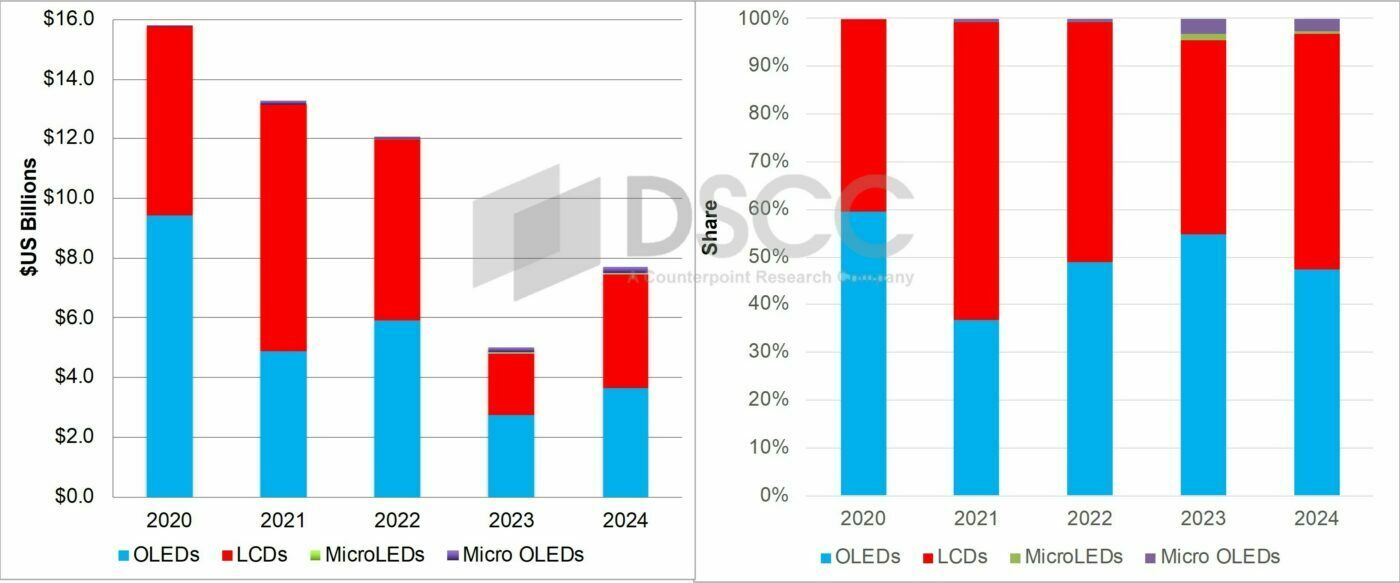

FPD製造装置設備投資は2023年に59%減となったが、2024年には54%増の77億ドルに回復する見通しだ。LCD設備投資が37億ドル・シェア49%でOLED設備投資の37億ドル・シェア47%を上回り、残りをMicro OLEDとMicroLEDが占める。

Display Equipment Spending to Rebound in 2024

※ご参考※ 無料翻訳ツール (Google)- Display equipment spending to jump 54% in 2024 after falling 59% in 2023.

- Samsung Display’s A6 fab to lead in spending in 2024 with a 30% share.

- Canon/Tokki to be the top supplier with a 13% share on over 100% growth.

After falling 59% in 2023, display equipment spending is expected to rebound in 2024, growing 54% to $7.7B. LCD spending is expected to outpace OLED equipment spending at $3.8B vs. $3.7B accounting for a 49% to 47% advantage with Micro OLEDs and MicroLEDs accounting for the remainder.

Display Equipment Spending and Share by Display Technology

In 2024, Samsung Display’s G8.7 IT OLED fab, A6, will account for the highest spending with a 30% share followed by Tianma’s TM19 G8.6 LCD fab with a 25% share and China Star’s t9 G8.6 LCD fab with a 12% share and BOE’s G6 LTPS LCD fab B20 with a 9% share. In total, Samsung Display is expected to lead in 2024 display equipment spending with a 31% share followed by Tianma at 28% and BOE at 16%. DSCC’s latest Quarterly Display Capex and Equipment Market Share Report forecasts out fab schedules by display technology through 2028.

Canon/Tokki is expected to lead with a 13.4% share on a delivery basis with their revenues up 100% to over $1B, leading the FMM VTE segment and #2 in exposure. Applied Materials is expected to hold the #2 position with an 8.4% share on 60% growth leading in CVD, TFE CVD, backplane ITO/IGZO sputtering and CF sputtering and 2nd in SEMs. Nikon, TEL and V Technology are expected to round out the top 5. Half of the top 15 are expected to enjoy over 100% growth in display equipment revenues.

IT fabs are expected to account for 78% of 2024 display equipment spending, up from 38%. Mobile is expected to account for the next highest share at 16%, down from 58%.

Oxide is expected to lead in 2024 equipment spending by backplane with a 43% share, up from 2% followed by a-Si, LTPO, LTPS and CMOS.

By region, China is expected to lead with a 67% share, down from 83%, followed by Korea with a 32% share, up from 2%.

DSCC’s Quarterly Display Capex and Equipment Market Share Report forecasts equipment spending by manufacturer, frontplane, backplane, glass size, application, substrate type, equipment type and equipment supplier out to 2027. For more information on this report, please contact info@displaysupplychain.com.

出典調査レポート Quarterly Display Capex and Equipment Market Share Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。