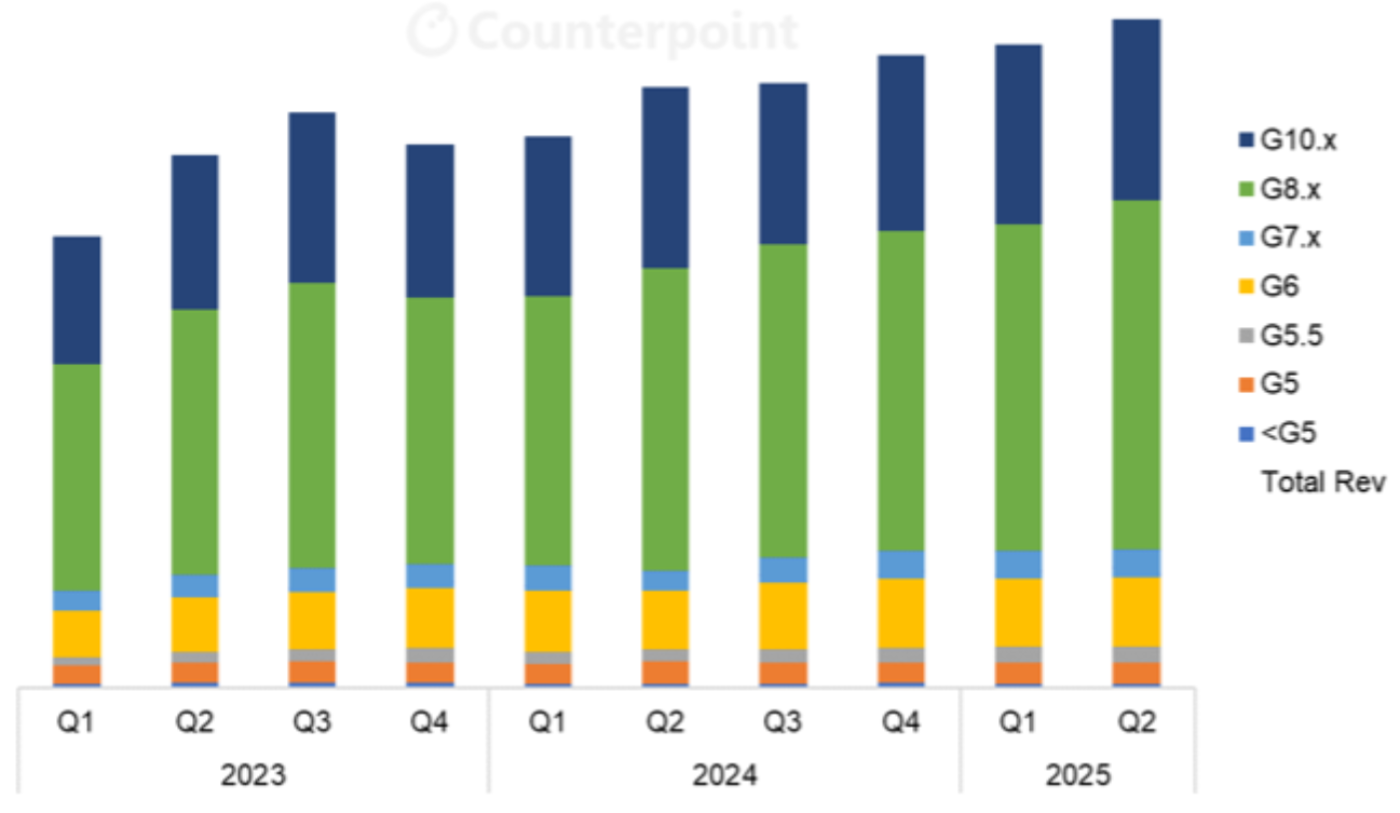

2025年上半期のFPD用ガラス出荷額は前年比14%増の見通し

出典調査レポート Quarterly Display Glass Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

記事のポイント

- Q4’24のFPD用ガラス出荷 (面積ベース) は前年比7%増、出荷額は16%増だった

- 2025年上半期のFPD用ガラス出荷額は前年比14%増の見通し

- 中国の国内ガラスメーカーが生産能力を増強しシェアを拡大している

2025年上半期のFPD用ガラス出荷額は前年比14%増の見通し

Counterpoint Researchが先週発刊した Quarterly Display Glass Report 最新版 によると、FPD用ガラス価格上昇と需要回復が相まって、2025年上半期のFPD用ガラス出荷額は前年比14%増となる見通しだ。FPD用ガラス基板メーカーとしてはCorningが引き続き優勢だが、価格上昇を主導したこと市場シェアが、特に中国でやや低下している。

FPD用ガラス基板出荷の推移 (日本円ベース)

ガラスはFPDにとって重要な材料であり、本レポートはその市場のあらゆる情報を網羅している。ガラス生産能力の詳細レビューをガラスメーカー別および地域別に提示するとともに、FPD用ガラス需要については、FPDメーカー/基板サイズ世代/バックプレーンタイプ/FPD技術/地域の各項目別に包括的に展望している。レポートではQ1’18からQ4’24までの四半期実績とQ1’25およびQ2’25の予測を提供している。

FPD用ガラス業界のQ4’24生産能力は前期比1%減・前年比2%増だった。CorningはSharpの第10世代工場閉鎖を受け、日本での生産を終了した。その一方で中国の国内ガラスメーカーは2023年から2024年にかけて第8.5世代生産能力を追加している。生産能力は依然として需要を大幅に上回っており、一部は遊休状態にある。

Q4’24のFPD用ガラス出荷は前期比2%減・前年比7%増だった。Q1’25は前期比2%増・前年比6%増、Q2’25は前期比4%増・前年比1%増と予測されている。

中国はFPD用ガラスにとって圧倒的な重要地域であり、Q4’24ガラス需要の75%を占めている。2025年上半期は中国のガラス需要が前年比9%増、台湾は同5%増が見込まれている。韓国のガラス需要が前年比13%減となる一方、Sharp堺第10世代工場の閉鎖により、日本のガラス需要は74%減となる見通しだ。FPD用ガラス市場における中国のシェアはQ2’25には過去最高の77%に達すると予測される。

Corning FPD用ガラス産業の草創期から業界をリードしてきたメーカーだが、FPD用ガラス市場における同社のシェアはQ4’24に低下している。同社のQ4’24のFPD用ガラス出荷は前年比5%減で、市場全体では5%増だった。最も大きく伸びているのはおもにIricoやTunghsu (別名Dongxu)など中国の小規模ガラスメーカーで、両社とも第8.x世代生産能力を増強している。

Corningは直近の決算報告で、2024年下半期にFPD用ガラス価格を2桁%引き上げることに成功したと発表した。FPD用ガラス価格は日本円で設定されており、Corningはここ数年の大幅な円安を値上げの正当な理由としている。Corningと競合する日本企業であるAGCとNEGもCorningに追随して値上げを実施しており、ガラスメーカー上位3社の間ではほぼ同水準の価格になっていると推定される。Q3’24には3%、Q4’24には7%の値上げがあったと推定され、Q1’25は価格が横ばいが予測される。

価格上昇により、FPD用ガラス出荷額は少なくとも日本円ベースでは増加しており、2025年も引き続き増加すると見られる。FPD用ガラス出荷額はQ4’24に前期比5%増・前年比16%増となっており、Q1’25は前期比1%増・前年比17%増、Q1’25は前期比4%増・前年比11%増が見込まれている。

出典調査レポート Quarterly Display Glass Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] Display Glass Revenues to Increase 14% YoY in H1 2025

- Display glass shipments increased 7% YoY in Q4 2024 and revenues increased 16%.

- Display glass revenues are expected to increase 14% YoY in the first half of 2025.

- Domestic Chinese glassmakers have added capacity and have gained share.

An increase in display glass prices combined with recovering demand will lead to a 14% YoY increase in display glass revenues in the first half of 2025, according to the latest update to Counterpoint Research’s Quarterly Display Glass Report, released last week. Corning continues to be the dominant supplier of display glass substrates, but its leadership on a price increase has led to some loss of market share, especially in China.

The display glass report covers all aspects of the market for this critical input for flat-panel displays. It provides a detailed review of glass capacity by glassmaker and by region, and a comprehensive view of display glass demand by panel maker, Gen size, backplane type, display technology and region. The report includes historical data by quarter from Q1 2018 to Q4 2024 and a forecast for Q1 2025 and Q2 2025.

Industry capacity for display glass decreased by 1% QoQ but increased 2% YoY in Q4 2024. Corning has shut down capacity in Japan after Sharp’s Gen 10 fab shutdown. On the other hand, domestic Chinese glass makers added Gen 8.5 capacity in 2023-2024. Capacity remains substantially higher than demand and some of it sits idle.

Glassmaker shipments of display glass decreased 2% QoQ but increased 7% YoY in Q4 2024. Shipments are expected to increase by 2% QoQ and 6% YoY in Q1 2025 and by 4% QoQ and 1% YoY in Q2 2025.

China is by far the most important region for display glass, accounting for 75% of glass demand in Q4 2024. We expect that glass demand in China will increase by 9% YoY in H1 2025 and by 5% YoY in Taiwan. Glass demand in South Korea will decrease by 13% YoY, while it will decrease in Japan by 74% due to the closure of Sharp’s Sakai Gen 10 fab. We expect that China’s share of the display glass market will reach an all-time high of 77% in Q2 2025.

Corning has been the leading supplier of display glass since the inception of the industry, but Corning’s share of display glass slipped in Q4 2024. Its shipments of display glass decreased 5% YoY in Q4 2024 whereas the total market increased by 5%. The biggest parties to gain were smaller glassmakers, primarily in China, including Irico and Tunghsu (aka Dongxu), as both companies have been increasing capacity in Gen 8.x sizes.

Corning stated in its recent earnings call that it had successfully implemented a double-digit % price increase for display glass in the second half of 2024. Display glass is priced in Japanese yen, and Corning justified the price increase by noting the substantial weakening of the yen in recent years. Corning’s Japanese competitors, AGC and NEG, have followed Corning’s lead and also increased prices, and we estimate that there is a rough price parity among the top three glassmakers. We estimate that prices increased 3% in Q3 2024 and 7% in Q4 2024, with flat prices expected in Q1 2025.

The higher prices mean that display glass revenues have been increasing, at least in JPY terms, and they will continue to increase in 2025. Display glass revenues increased by 5% QoQ and 16% YoY in Q4 2024, and we forecast revenues to increase 1% QoQ and 17% YoY in Q1 2025 and 4% QoQ and 11% YoY in Q2 2025.