FPD設備投資予測を上方修正~OLEDメーカーが能力増強で需要増に対応

出典調査レポート Quarterly Display Capex and Equipment Market Share Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

記事のポイント

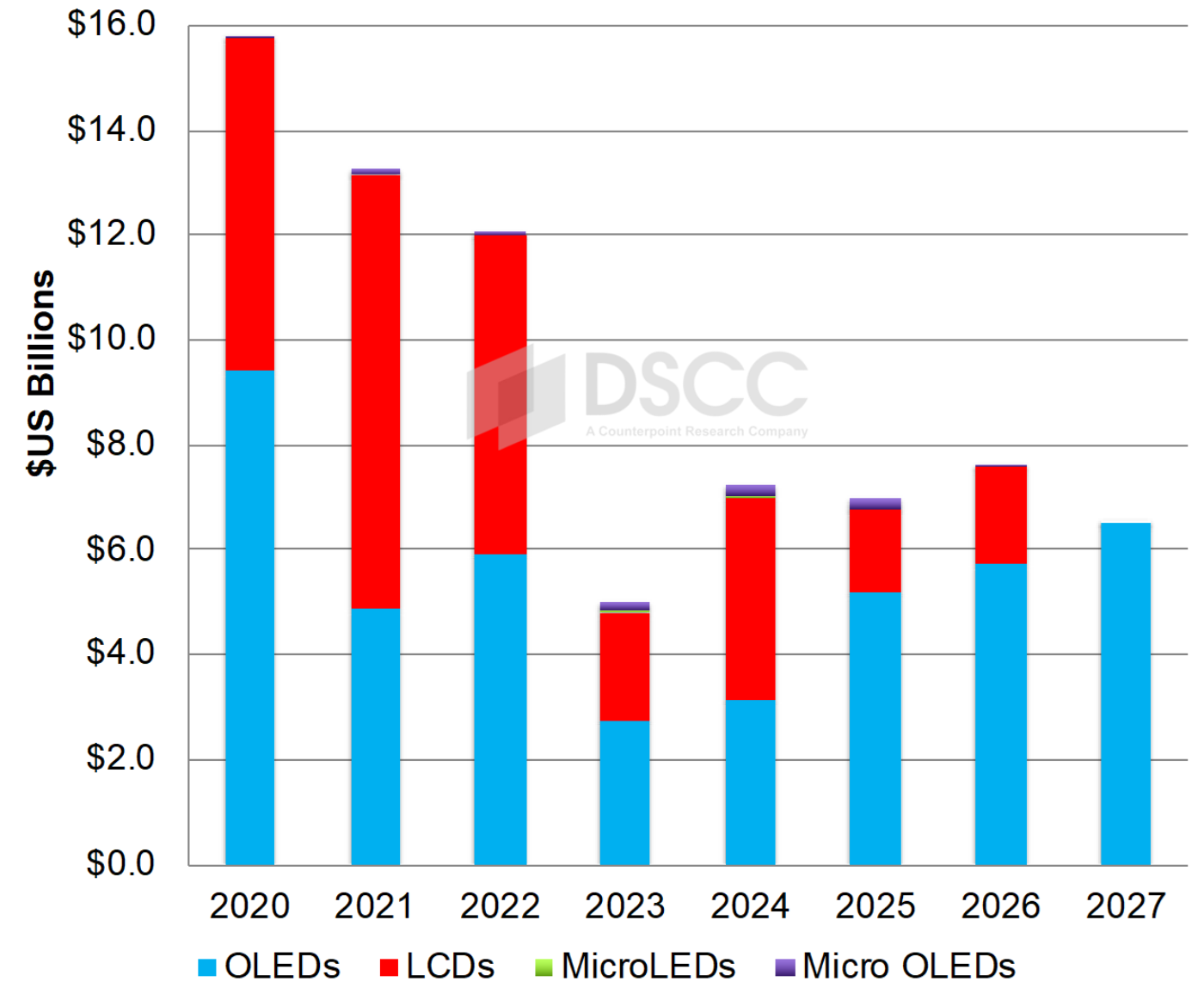

- DSCCは2020年-2027年のFPD設備投資 (建屋は含まない製造装置ベース) の累計予測を、前回 (Q2'24版) 予測から8%増の750億ドルに上方修正した。OLEDは需要増と稼働率上昇に能力増強で対応するため、設備投資が14%増の440億ドルになる。LCD、Micro OLED、MicroLEDは横ばい。

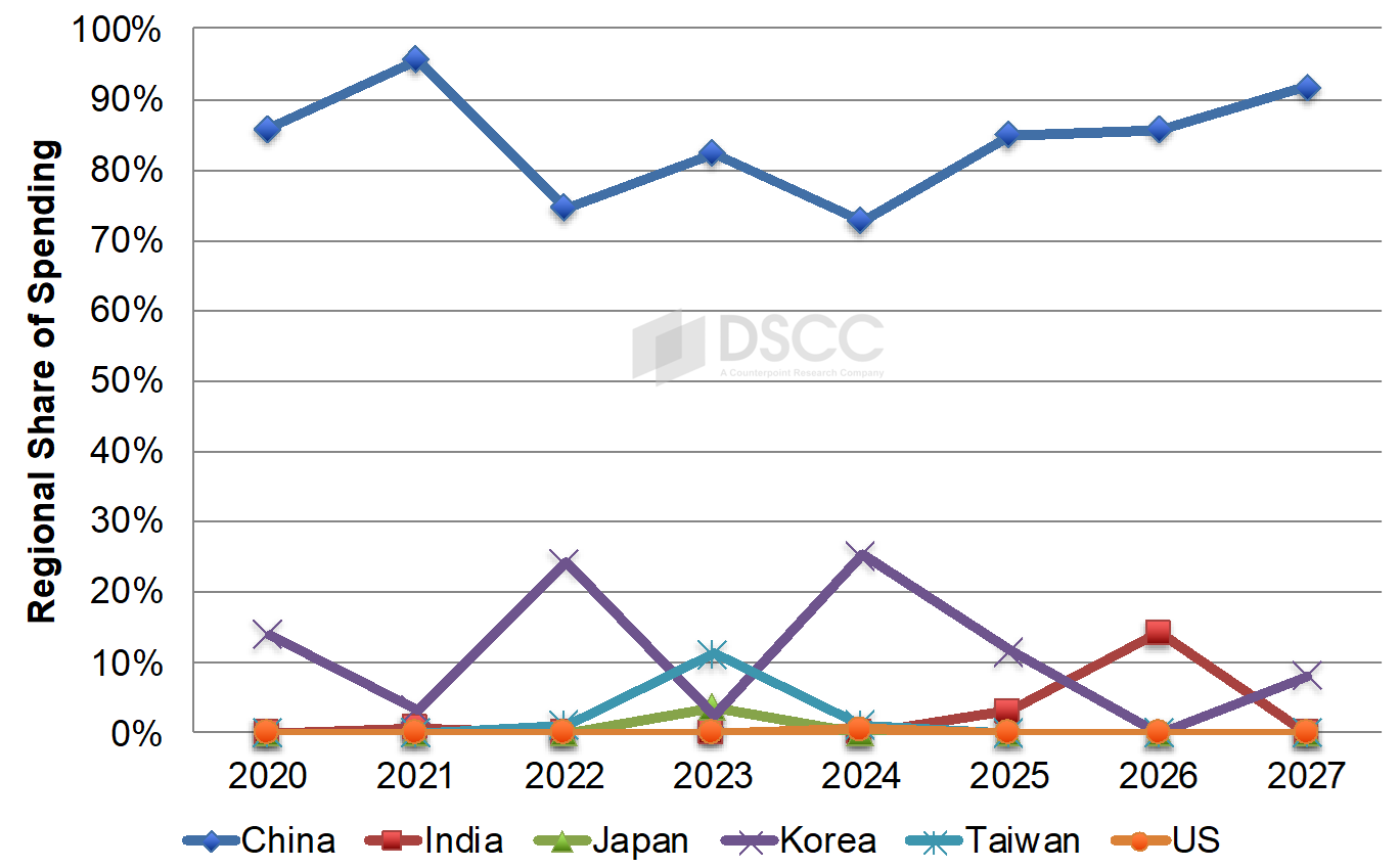

- 中国が2020年-2027年のFPD製造装置投資の85%を占め、いずれの年も首位に立つと予測される。中国のシェアは、LCDでは92%、OLEDでは77%、Micro OLEDでは80%である。

- 用途別ではITが最も高いシェアを占めると予測される。設備投資はBOEが首位、China StarとTianmaが続く。Canon/Tokkiが製造装置メーカー首位の座を維持、Applied MaterialsとNikonが続く。

DSCCが Quarterly Display Capex and Equipment Market Share Report 最新版で、2020年-2027年のFPD設備投資 (建屋は含まない製造装置ベース) の累計予測を、前回 (Q2'24版) 予測から8%増の750億ドルに上方修正した。OLED設備投資が14%増の440億ドルになることが今回の予測の根拠となっている。LCDは300億ドルで横ばい、Micro OLEDとMicroLEDも横ばいの見通しである。

OLED設備投資増加の大きな要因は、3つの第6世代モバイル用ラインの追加、従来予測にはなかった第8.7世代IT用OLEDラインの7.5K追加拡張、さらに15Kの第8.7世代IT用OLEDラインの1年前倒しによるものである。OLED設備投資は2023年から2027年まで毎年増加し、需要増と稼働率上昇により2027年には65億ドルに達すると予測される。OLEDの普及はスマートフォン、タブレット、ノートPC、その他の市場で拡大し続けており平均パネルサイズも継続的に成長、稼働率が過剰な水準に達すると予測される場合、FPDメーカーは能力追加を促されることになる。2020年-2027年のFPD設備投資ではOLEDが需要増とLCDよりも高い資本集約度によってシェア58%に達すると予測される一方、LCD生産ラインのシェアは40%になる見通しで、2024年-2027年に新規追加が現在予測されているLCD生産ラインは4つだけである。

フロントプレーン別FPD設備投資予測

地域別では、2020年-2027年設備投資に対する中国のシェア予測は83%から85%に上昇、累計630億ドルで、毎年中国が首位に立つ見通しだ。この期間の韓国のシェア予測は13%から12%に低下、累計90億ドルになると見られる。インドはシェア2%、台湾はシェア1%と予測される。また、同期間の中国のシェアは、LCDでは92%、OLEDでは77%、Micro OLEDでは80%が予測されている。

地域別FPD設備投資シェア予測

用途別ではITが300億ドル・シェア41%で首位に立つと見られ、250億ドル・シェア37%で2024年から2027年の首位という従来予測から引き上げとなっている。IT需要はまだ2021年水準を大きく下回っており、先進FPD技術のIT用生産ラインが稼働可能になれば旧型a-Si生産ラインは圧迫され、旧型ラインの閉鎖が増えると見られる。新規ライン3つが追加されるモバイル用設備投資が220億ドル・シェア30%で用途別第2位、TV/その他が210億ドル・シェア28%になると予測される。モバイルは2022年と2023年、TVは2020年と2021年の首位だった。AR/VR設備投資はTFTバックプレーンおよびOLEDフロントプレーンセグメントで10億ドル未満・シェア1.2%と予測される。

FPDメーカー別では、BOEがシェア23%で首位に立ち、以下China Starがシェア20%、Tianmaがシェア11%、HKCとVisionoxがそれぞれシェア10%、SDCがシェア7%、LGDがシェア5%で続くと予測される。BOEはOLED分野をシェア27%で、China StarはLCD分野をシェア30%でリードする見通しだ。Micro OLED設備投資ではSidtekがシェア25%でリードすると予測される。

製造装置メーカー別では、Canon/Tokkiが30%成長で首位の座を維持するが、予測シェアは10.3%から9.3%に下がる。Applied Materialsは52%成長でシェアは8.1%から8.5%に上がる見通しだ。Nikonは第3位維持の見込みで、LCD露光装置分野を独占、OLED市場をCanonと分け合うと予測される。製造装置メーカー上位15社のうち8社で100%以上の成長が見込まれる。上位15社を国別に見ると、日本が8社、韓国が4社、中国が2社、米国が1社となる。

------------------------------------

Quarterly Display Capex and Equipment Market Share Report では70以上のFPD装置セグメントで出荷額を追跡し各セグメントの市場シェアを提示しています。また、各種FPD製造装置メーカー170社以上のデータを各セグメントのデザインウィンとともに明らかにしています。FPD製造装置、生産能力、製造装置市場シェアに関する詳細データはレポートをご覧ください。

[原文] DSCC Raises Capex Outlook as OLED Manufacturers Respond to Rising Demand with More Capacity

- DSCC raised its 2020-2027 display equipment spending forecast by 8% to $75B due to a 14% increase in OLED spending to $44B as manufacturers respond to rising demand and elevated utilization with additional capacity. LCD, Micro OLED and MicroLED spending held flat.

- China is expected to account for 85% of display equipment spending from 2020-2027, leading annually. Its share of LCD spending is 92% with OLEDs at 77% and Micro OLEDs at 80%.

- IT applications expected to account for the highest share of spending. BOE to lead in equipment spending followed by China Star and Tianma. Canon/Tokki to remain the #1 supplier followed by Applied Materials and Nikon.

DSCC raised its display equipment spending forecast from 2020-2027 in its latest Quarterly Display Capex and Equipment Market Share Report by 8% to $75B due to a 14% increase in OLED spending to $44B. LCD spending remained flat at $30B while Micro OLED and MicroLED spending also remained flat.

The OLED increase can primarily be attributed to the addition of three G6 mobile lines, an additional 7.5K expansion at a G8.7 IT OLED line not previously forecasted and the pull-in by a year of another 15K G8.7 IT OLED line. OLED equipment spending is expected to increase each year from 2023 to 2027 reaching $6.5B in 2027 due to increased demand and rising utilization. OLED penetration continues to increase in smartphone, tablet, laptop and other markets with average panel sizes continuing to grow encouraging panel suppliers to add capacity when utilization is forecasted to reach excessive levels. While OLEDs are expected to account for a 58% share of 2020-2027 display equipment spending on rising demand and higher capital intensity than LCDs, LCD fabs are expected to account for a 40% share with just four new LCD fabs currently forecasted to be equipped from 2024-2027.

By region, China’s share of 2020-2027 spending is projected to be 85%, up from 83%, on $63B spent, with China leading every year. Korea’s share of spending over this period is expected to be 12%, down from 13%, on $9B spent. India is expected to account for a 2% share with Taiwan at 1%. China is also expected to dominate LCD spending with a 92% share over the same period with OLED regional spending with a 77% share and Micro OLED spending with an 80% share.

By application, IT markets are expected to lead with a 41% share on $30B in spending, up from a 37% share on $25B in spending and leading from 2024-2027. With IT demand still well below 2021 levels, we expect these fabs with more advanced display technology to pressure older a-Si fabs once they come online leading to additional older fab closures. With the addition of three new mobile lines, mobile is expected to be the #2 application with a 30% share on $22B in spending followed by TV/Other with $21B and a 28% share. Mobile led in 2022 and 2023 while TVs led in 2020 and 2021. AR/VR is expected to account for a 1.2% share on less than $1B in spending tracking TFT backplane and OLED frontplane segments.

By panel manufacturer, BOE is expected to lead with a 23% share followed by China Star at 20%, Tianma at 11%, HKC and Visionox at 10% each, SDC at 7% and LGD at 5%. BOE is also expected to lead in OLEDs with a 27% share with China Star leading in LCDs with a 30% share. In Micro OLEDs, Sidtek is expected to lead with a 25% share.

By equipment supplier, Canon/Tokki is expected to remain #1 on 30% growth and a 9.3% share, down from 10.3%. Applied Materials is expected to enjoy 52% growth and gain share from 8.1% to 8.5%. Nikon is expected to remain #3, dominating LCD exposure and splitting the OLED market with Canon. Eight of the top 15 equipment suppliers are expected to enjoy >100% growth. By country within the top 15, there are expected to be eight from Japan, four from Korea, two from China and one from the US.

Equipment revenues are tracked for over 70 different display equipment segments with market share provided for each one. Over 170 different equipment supplies are identified with design wins by segment. For more insights regarding display equipment, capacity and equipment market share, please see our Quarterly Display Capex and Equipment Market Share Report.

出典調査レポート Quarterly Display Capex and Equipment Market Share Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。