FPD需給予測~FPD供給過剰の終わりとLCD不足の始まり

出典調査レポート Quarterly FPD Supply/Demand Report (日本独自仕様版) の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

- 2023年-2028年のFPD需要は年平均成長率5%と予測される。おもな要因はTV画面サイズの大型化

- OLED生産能力は年平均成長率5%が予測される一方、2022年-2028年のLCD生産能力は年平均成長率1%未満が予測される

- 需要の高まりがLCD生産ライン稼働率を押し上げ、LCD生産能力の追加がなければ、パンデミック時の高水準を上回ると見られる

需要急増時に生産能力が追加されたため、FPD業界では2024年まで供給過剰状態が続いているが、いずれは供給不足に転じることになる。その転換点は、DSCCが発刊した Quarterly FPD Supply/Demand Report ※日本独自仕様版はこちら によると、予測期間である5年以内に起こると見られる。FPD製品需要は緩やかな成長にとどまると予測されるが、その持続的な成長によって生産能力が満たされ、いずれは新たなLCD生産ラインの建設や拡張の需要をもたらすだろう。

Quarterly FPD Supply/Demand Report ※日本独自仕様版はこちら は需要と供給の両面を対象にFPD業界の包括的見解を提供している。需要予測では、8用途のFPD出荷をLCDとOLEDの各技術別に予測している。

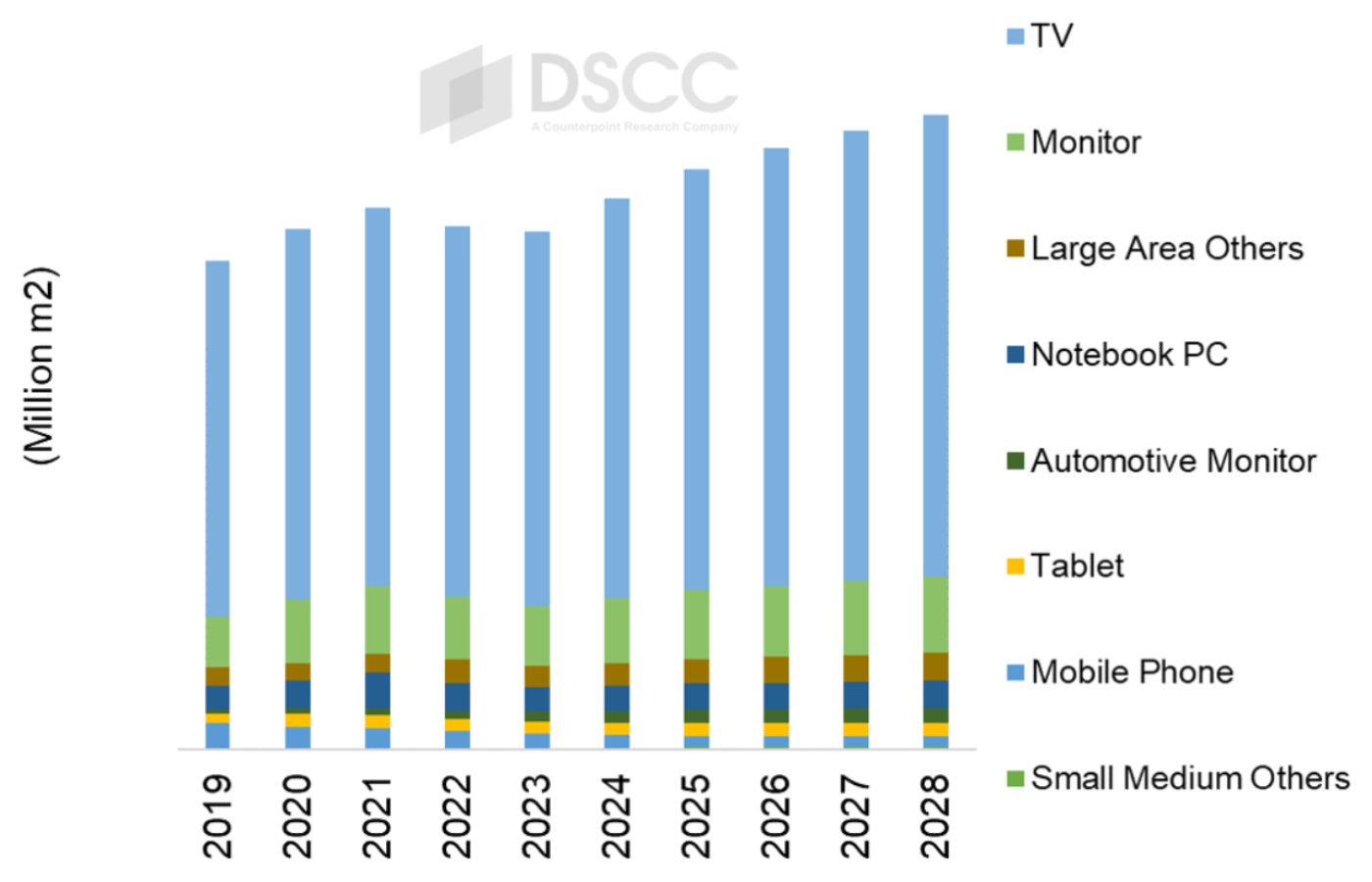

FPD業界を理解する上で出荷数と出荷額は重要だが、需給を把握する上で最も重要な意味を持つのが面積だ。2022年と2023年はパンデミックの余波でFPDの面積需要が2年連続で減少したが、その後2024年になって成長が再開しており、2023年-2028年は年平均成長率5%で成長が続くものと予測されている。

TVがFPD需要の大部分を占める状況は今後も変わらず、TVの面積需要は平均画面サイズの拡大と数量の増加にともなって成長していくと見られる。また、IT市場がパンデミック後の低迷から回復するにしたがい、IT用途 (モニター、ノートPC、タブレット) の面積成長も期待される。

用途別 FPD面積需要

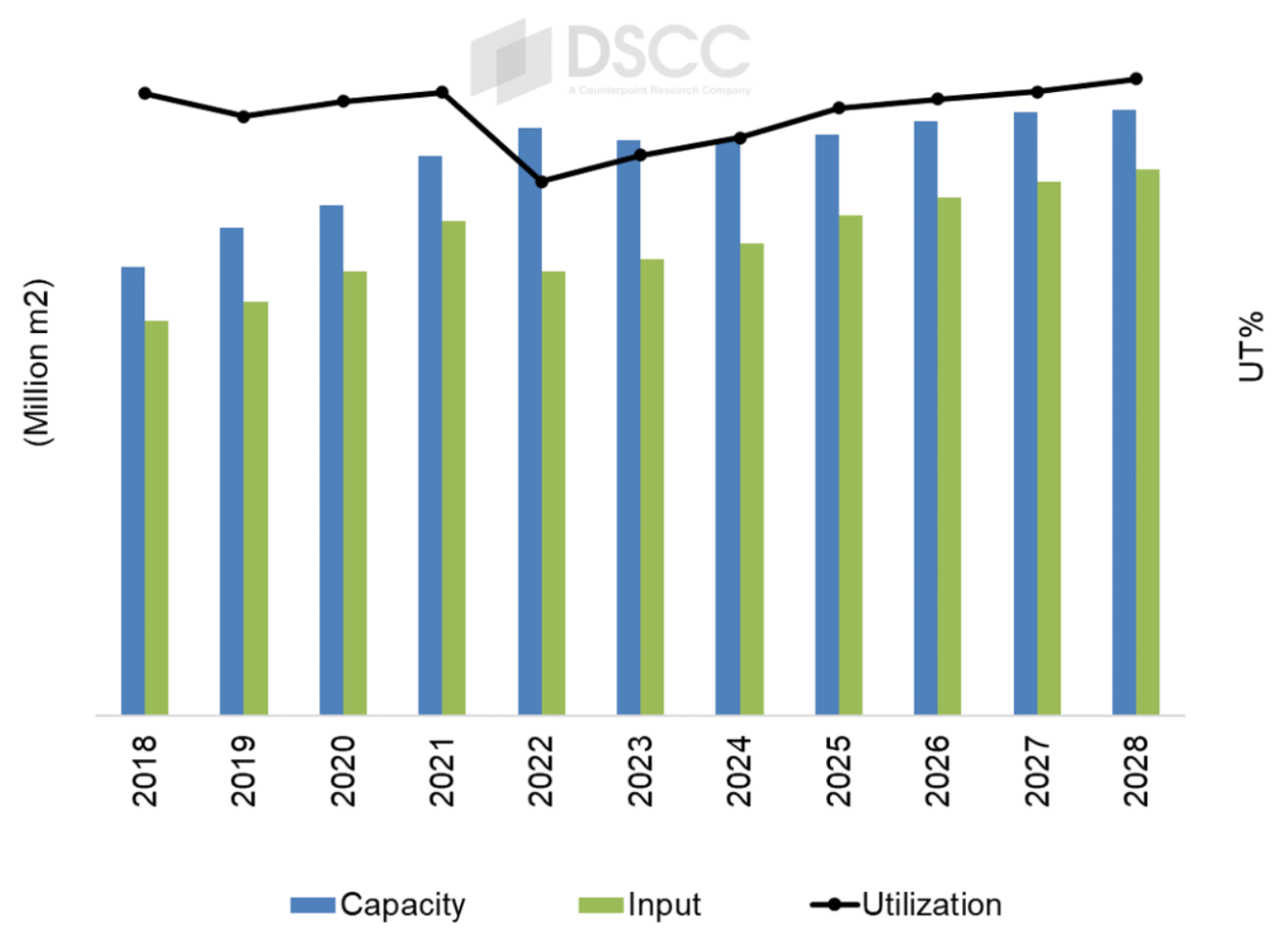

Quarterly FPD Supply/Demand Report ※日本独自仕様版はこちら にはDSCCによる詳細な生産能力予測も掲載しており、LCDとOLEDの生産能力に関する見解を、基板世代別、FPDメーカー別、生産地域別に提供している。2023年は一部の小規模生産ラインの閉鎖によってLCD生産能力が2%減となった。

全般的に見ると、2022年-2028年のLCD生産能力は第7世代以下ラインで縮小の一方、第8.x世代以上のラインでは成長が見込まれている。その結果、2022年-2028年のLCD生産能力の年平均成長率は1%未満になると予測されている。

LCD業界はパンデミックによる高騰後の2022年に底を打ったが、以降は毎年わずかに改善している。2022年の低稼働率は莫大な営業損失を示唆するものとなったが、2023年はわずかながら改善し、2024年はまだ終わっていないものの、通年の稼働率は2023年よりも高くなると予測されている。

最小限の生産能力の追加と安定した需要の伸びにより、LCDメーカーの収益性は2025年と2026年も改善が続く見通しだ。現在の需給展望から、2027年の稼働率はパンデミックのピーク年である2021年と同水準になり、2028年にはさらに上昇するとDSCCでは予測している。稼働率がこのような水準にあるとLCD価格が急騰し供給増の圧力が生まれることになる。OLED生産能力の追加で需要に対応することも考えられるが、ギャップを埋めるにはOLEDメーカーの拡張計画は倍増以上が必要になる。

LCD需給予測 (全世代および全用途)

------------------------------------

DSCCの Quarterly FPD Supply/Demand Report ※日本独自仕様版はこちら では、8用途を対象としたLCDおよびOLED需要推移を網羅的に提供するとともに、各用途の出荷数、出荷面積、出荷額を予測しています。また、FPD技術別、地域別、世代サイズ別に業界の生産能力を提示し、業界の各セグメントの需要と供給の比較も行っています。

出典調査レポート Quarterly FPD Supply/Demand Report (日本独自仕様版) の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] DSCC Report Projects the End of Flat Panel Display Oversupply and Beginning of LCD Shortage

- DSCC forecasts flat panel display demand CAGR of 5% from 2023-2028, driven mainly by increasing TV screen size.

- While OLED capacity is expected to grow with a 5% CAGR, LCD capacity CAGR from 2022-2028 is less than 1%.

- Rising demand will push LCD fab utilization above pandemic high levels unless more LCD capacity is added.

Capacity additions put in place during the pandemic demand boom have resulted in a systematic oversupply in the display industry that continues in 2024, but that oversupply will eventually turn to a shortage. That turn will happen within the 5-year timeframe of our forecast, according to DSCC's Quarterly FPD Supply/Demand Report, released last week. Although we expect only modest growth in demand for display products, that persistent growth will fill up capacity and will eventually lead to demand for new or expanded LCD fabs.

The Quarterly FPD Supply/Demand Report gives a comprehensive view of the display industry because it covers both the demand and supply sides. The demand forecast covers flat panel display shipments across eight different applications, with technology split between LCD and OLED.

While units and revenue are important to understanding the display industry, the most meaningful metric for supply/demand is area. After two consecutive years of pandemic hangover where FPD demand area decreased in 2022-2023, we are seeing growth resume in 2024 and expect it to continue through 2028 with a 2023-2028 CAGR of 5%.

TVs will continue to represent a dominant share of FPD demand, and area demand for TVs will grow primarily from increasing average screen size along with incremental unit growth. We also expect area growth from IT applications (Monitor, Notebook, Tablet) as the IT market recovers from its post-pandemic slump.

The Quarterly FPD Supply/Demand Report covers DSCC’s detailed capacity forecast, giving views of LCD and OLED capacity by Gen Size, by supplier and by production region. LCD capacity decreased in 2023 by 2% as some smaller fabs shut down.

Overall, we expect that LCD capacity in Gen 7 and smaller fabs will decrease over the span 2022-2028, while capacity in Gen 8.x and larger will grow, with the net result that LCD capacity CAGR from 2022-2028 will be less than 1%.

The LCD industry hit a low point in 2022 following the pandemic high but has improved a bit each year since then. The low utilization in 2022 meant huge operating losses, but 2023 was a little better, and although 2024 is not complete, we expect full-year utilization to come in higher than 2023.

With minimal capacity additions planned and steady demand growth, LCD makers’ profitability is likely to continue to improve in 2025 and 2026. Based on the current supply/demand outlook, we expect utilization in 2027 to be equal to the pandemic peak year UT% in 2021, and UT% to be even higher in 2028. At such utilization levels, LCD panel prices would spike, creating pressure for more supply. Although additional OLED capacity could help meet demand, the expansion plans of OLED makers would need to more than double to fill the gap.

As noted above, the DSCC's Quarterly FPD Supply/Demand Report provides a comprehensive listing of historical panel demand in LCD and OLED for eight different applications, plus a forecast of units, area, and revenues for each application. The report gives a view of industry capacity by display technology, region and gen size, and gives a comparison of supply and demand across segments of the industry.