Q2’24のフォルダブル型スマートフォン用パネル出荷数は過去最高記録の見込み~調達はSamsungがHuaweiから、出荷はSDCがBOEから首位奪還へ

出典調査レポート Quarterly Foldable/Rollable Display Shipment and Technology Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEBご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

記事のポイント

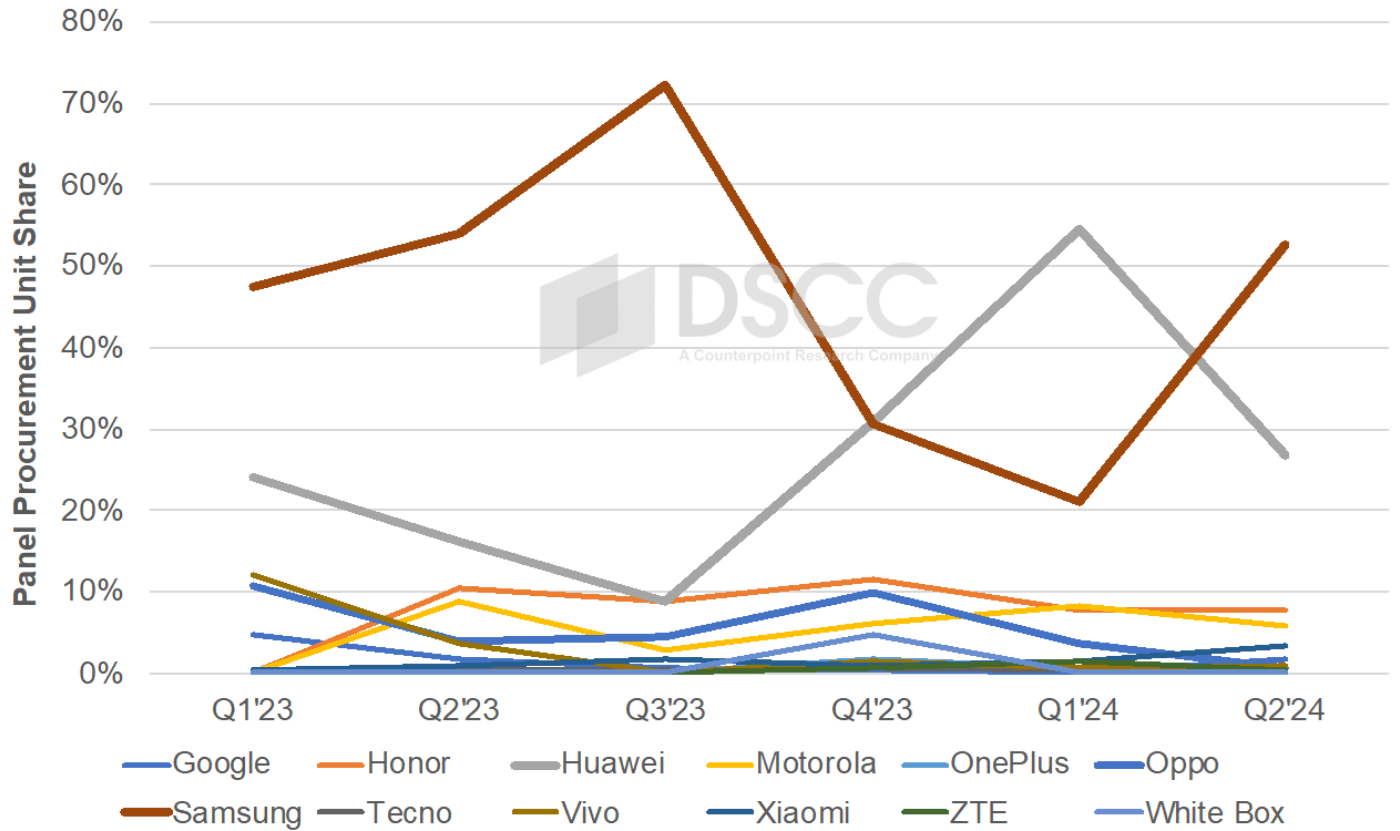

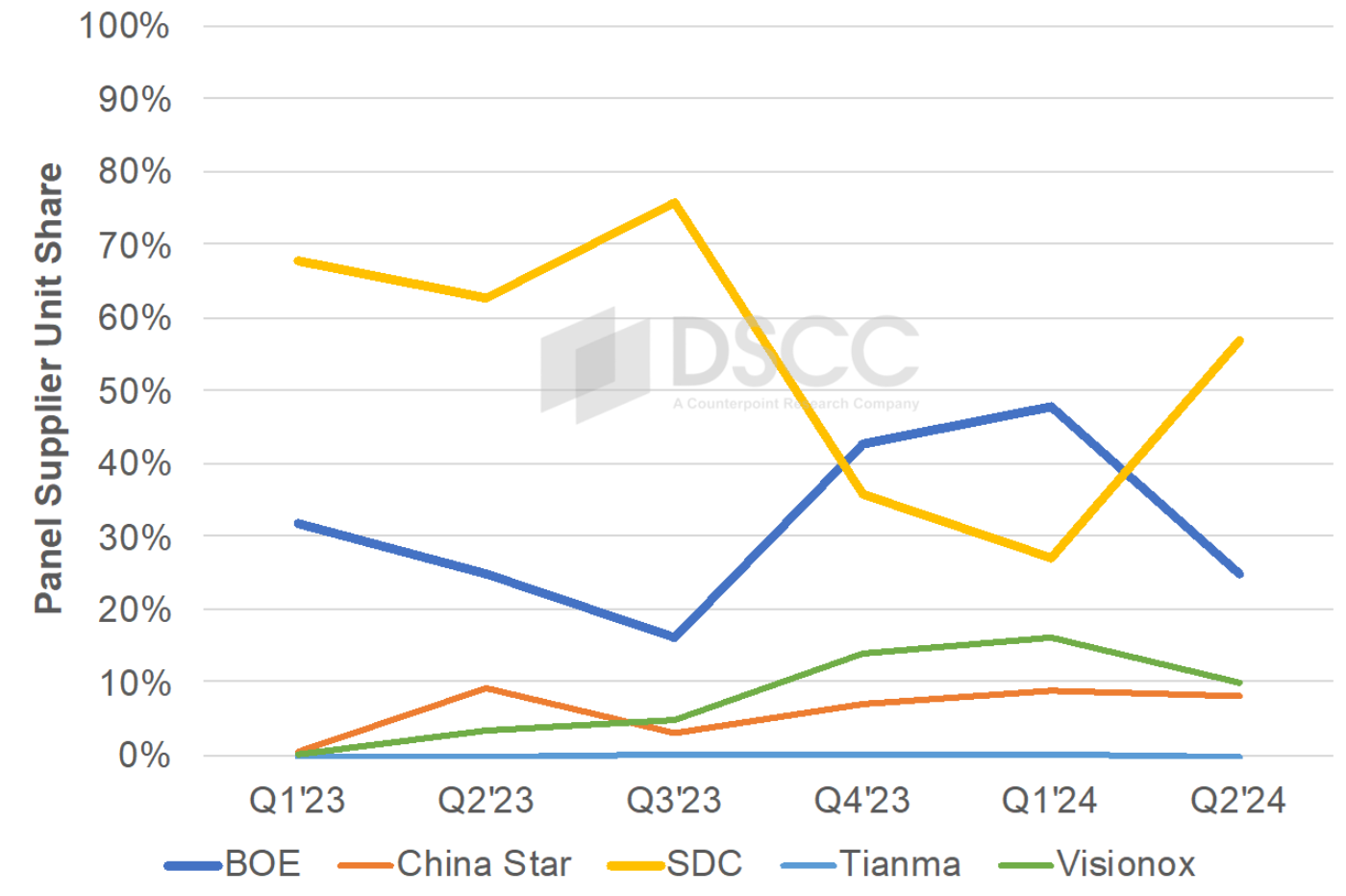

- Q1'24のフォルダブル型スマートフォン用パネル出荷数は前年比46%増だった。パネル調達数ではHuaweiが過去最高のシェア55%で優勢、2四半期連続の首位となった。パネル出荷数ではBOEがシェアを43%から48%に上げ、同じく2四半期連続の首位となった。フォルダブル型スマートフォン用パネル調達ベースでは、HuaweiのMate X5とPocket 2が上位2機種となった。

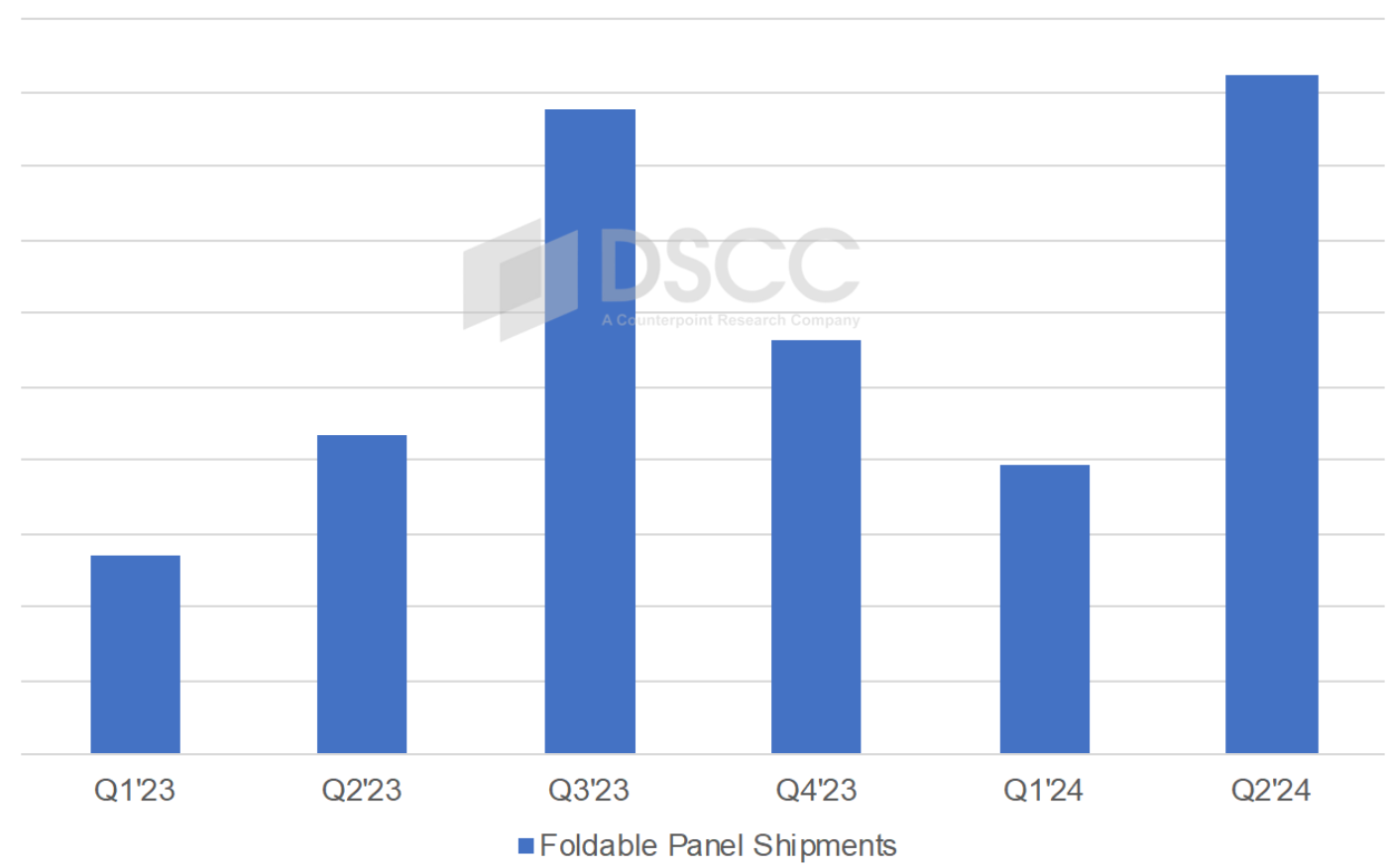

- Q2’24のフォルダブル型スマートフォン用パネル出荷数は、前年比113%増の925万枚で過去最高を記録すると予測される。Samsungが最新のZ FlipおよびZ Fold向けパネル調達/生産を昨年より1ヵ月前倒し、Huaweiでは新機種と中国の旺盛な需要でパネル調達が引き続き伸びていることが要因である。Q2’24はSamsungのGalaxy Z Flip 6とZ Fold 6がフォルダブル型スマートフォン用パネル調達ベースで上位2機種になると予測される。

- 2024年通年では、SamsungとSamsung Displayが、2023年よりは縮小するものの、大きな優位性を維持すると予測される。

Q1'24のフォルダブル型スマートフォン用パネル出荷数は前年比46%増の394万枚だった。Q1'24はHuaweiがフォルダブル型スマートフォン用パネル調達数で過去最高となるシェア55%を獲得、HuaweiのMate X5およびPocket 2向けフォルダブル型パネルがQ1'24調達数全体の50%以上を占めた。HuaweiはQ4’23にフォルダブル型スマートフォン用パネル調達数でSamsungをわずかに上回り、Q1'24で2四半期連続の首位となった。Q1'24のパネル調達の対象となったフォルダブル型スマートフォンは24機種だった。

Q1'24はフォルダブル型スマートフォン市場にとって季節的に低調な四半期だったが、Q2'24はSamsung Displayから最新のZ FlipおよびZ Foldモデル向けパネル出荷が昨年より1ヵ月早く、5月ではなく4月に開始、Huaweiのパネル調達も引き続き増加していることから、フォルダブル型スマートフォン用パネル調達数は925万枚となり過去最高を更新すると予測される。Q2'24のパネル調達数ではSamsungがシェア52%でHuaweiのシェア27%を上回ると見られ、今後発売予定のZ Flip 6とZ Fold 6がパネル調達ベースで最多の2機種となる見通しだ。Huaweiのモデルはパネル調達ベースで第3位、第4位、第6位となるだろう。Q2'24のパネル調達対象は27機種になる見通しである。ただし、セルイン (販売台数) ベースではQ2'24もHuaweiがリードを維持するだろう。

フォルダブル型スマートフォン用パネル出荷数

フォルダブル型スマートフォン用パネル ブランド別調達シェア

フォルダブル型スマートフォン用パネル FPDメーカー別シェア

2024年通年では、フォルダブル型スマートフォン用パネル調達ベースでのSamsungのシェアは1300万枚超で54%から48%に低下、続くHuaweiは18%から28%に上昇、Honorが9%から10%に上昇となる見通しだ。パネル調達対象モデル数は2023年の35機種から2024年には38機種に増加が見込まれる。トップ10モデルのうち、Samsungが3機種、Huaweiが4機種、HONORが2機種を占めると予測される。

FPDメーカー別シェアでは、Q4’23とQ1’24はBOEがSamsung Display (SDC) をリードしたが、Q2'24はSDCがシェア57%でBOEのシェア25%を上回り、Z Flip 6とZ Fold 6が立ち上がるQ3'24にはさらに差が広がると見通しだ。2024年通年では、SDCがシェア54%でシェア28%のBOEをリードすると予測される。SDCのシェアは2023年の62%から低下、BOEのシェアは2023年の27%から上昇となる。2024年はVisionoxが最もシェアを伸ばし11%に到達、China Starは7%への上昇が予測される。

DSCCの Quarterly Foldable/Rollable Display Shipment and Technology Report は、スマートフォン/ノートPC/タブレット/TV市場向けのフォルダブルパネルおよびローラブル/スライド式パネルの出荷を追跡、予測しています。また、Counterpoint Researchによる地域別およびブランド別地域別セルイン実績とブランド別およびモデル別セルイン予測も掲載しています。さらに、主要ディスプレイ技術/機能および重要半導体部品に関する各種パラメータ別出荷データ、モデル別パネル価格実績および予測、その他の情報を掲載しています。

出典調査レポート Quarterly Foldable/Rollable Display Shipment and Technology Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEBご試読は こちらから お問い合わせください。

[原文] Foldable Smartphone Panel Volumes Expected to Reach an All Time High in Q2’24, Samsung and Samsung Display Expected to Wrestle Leadership Away from Huawei and BOE

- Q1’24 foldable smartphone panel shipments rose 46% Y/Y. Huawei dominated panel procurement with a 55% share, its highest ever, and led for the second consecutive quarter. BOE led in foldable panel shipments for the second consecutive quarter with a 48% share, up from 43%. The Huawei Mate X5 and Pocket 2 were the top two models on a foldable panel procurement basis.

- Q2’24 foldable smartphone panel shipments are expected to rise 113% Y/Y to a record high 9.25M as Samsung pulls in procurement/production for its latest Z Flip and Z Fold panels by a month from last year and Huawei’s panel procurement continues to grow on new models and strong demand in China. The Samsung Galaxy Z Flip 6 and Z Fold 6 are expected to be the top two models in Q2’24 on a foldable panel procurement basis.

- For all of 2024, Samsung and Samsung Display are expected to maintain large advantages although narrower than in 2023.

Foldable smartphone panel shipments rose 46% Y/Y in Q1’24 to 3.94M. Huawei dominated foldable smartphone panel procurement in Q1’24 with a 55% share, its highest ever, with the Huawei Mate X5 and Pocket 2 accounting for over 50% of all foldable panels purchased in Q1’24. Q1’24 was the second consecutive quarter Huawei led in foldable smartphone panel procurement after holding a slight edge over Samsung in Q4’23. There was panel procurement for 24 different foldable smartphone models in Q1’24.

While Q1’24 was a seasonally slow quarter for the foldable market, Q2’24 is projected to establish a new record high for foldable smartphone panel procurement at 9.25M as Samsung Display starts panel shipments for its latest Z Flip and Z Fold models one month earlier than last year, in April rather than May, and Huawei’s panel procurement continues to grow. In Q2’24, Samsung is expected to hold a 52% to 27% advantage over Huawei in panel procurement with the upcoming Z Flip 6 and Z Fold 6 the two highest volume models on a panel procurement basis. Huawei will have the #3, #4 and #6 models on a panel procurement basis. There is expected to be panel procurement for 27 different models in Q2’24. On a sell-in basis for Q2’24, Huawei will still lead, however.

For all of 2024, Samsung’s share of foldable smartphone panel procurement is expected to fall from 54% to 48% at over 13M panels, followed by Huawei with a 28% share, up from 18% and Honor with a 10% share, up from 9%. There is expected to be panel procurement for 38 different models in 2024, up from 35 in 2023. Samsung is expected to account for three models in the top 10 with Huawei accounting for four and Honor accounting for two.

In terms of panel supplier share, while BOE led Samsung Display (SDC) in Q4’23 and Q1’24, SDC is expected to hold a 57% to 25% advantage in Q2’24 over BOE and an even larger advantage in Q3’24 as the Z Flip 6 and Z Fold 6 ramp. For all of 2024, SDC is expected to lead BOE with a 54% to 28% share advantage. SDC’s share will be down from 62% in 2023 with BOE’s share up from 27% in 2023. Visionox is expected gain the most share in 2024 reaching 11% with China Star rising to 7%.

DSCC’s Quarterly Foldable/Rollable Display Shipment and Technology Report tracks and forecasts panel shipments for foldable and rollable/slidable panels in the smartphone, notebook, tablet and TV markets. It also now includes sell-in data results by region and by brand/region from Counterpoint Research along with sell-in forecasts by brand and model. It also includes shipments by parameter for critical display technologies and features as well as critical semiconductor components, panel price results and forecasts by model and much more.