Q1'24のOLED出荷数は前年比50%増~スマートフォン/TV/スマートウォッチ/IT用途が前年比プラス成長

出典調査レポート Quarterly OLED Shipment Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

記事のポイント

◆Q1'24のOLED出荷数は前年比50%増、モニターとタブレットがけん引した。◆Q1'24にはスマートフォン用OLEDとTV用OLEDは季節要因のため前期比で減少したが、前年比では増加している。◆Q1'24にはスマートフォン用OLEDで複数ブランドが前期比2桁成長を達成した。

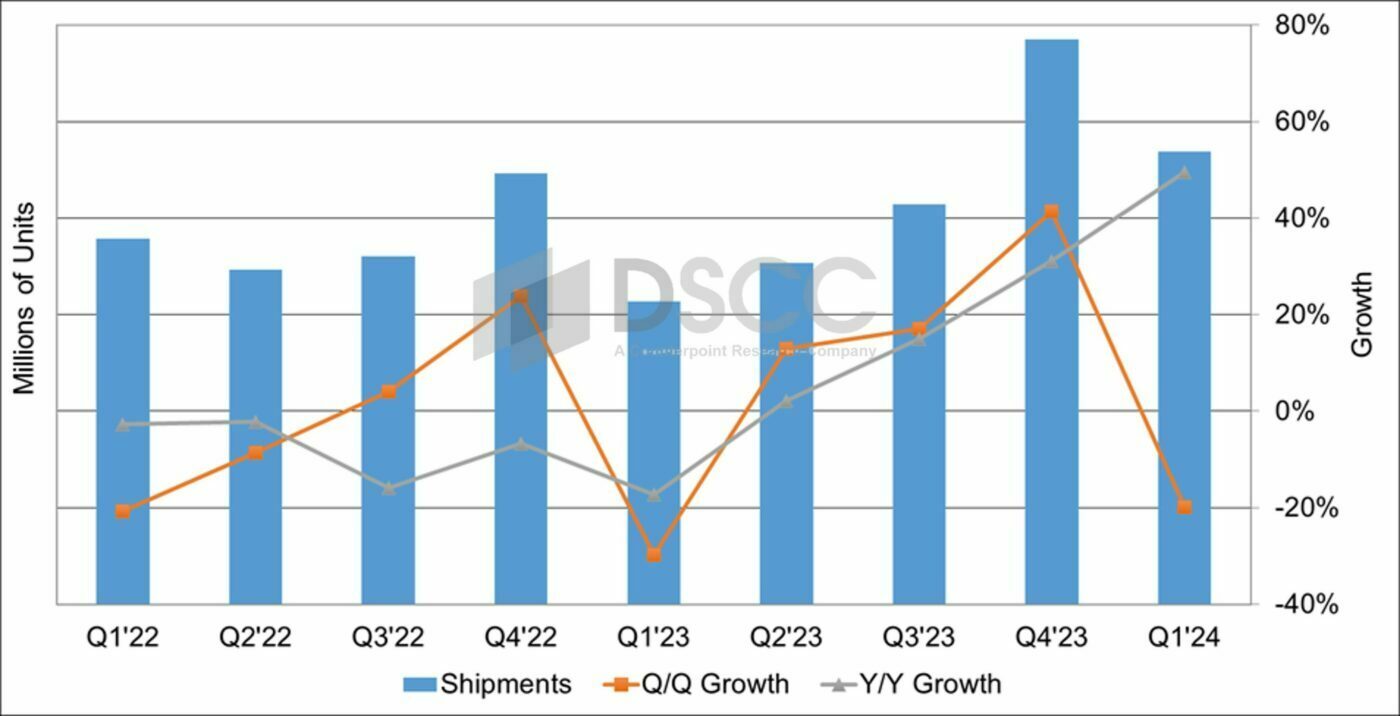

DSCCが発行した最新の Quarterly OLED Shipment Report 速報版によると、OLED出荷数はQ4'23に前期比41%増・前年比31%増となり、続くQ1'24に前期比20%減・前年比50%増となった。Q1'24実績を主要OLED用途別に見ると、モニター用OLED出荷は前期比35%増・前年比189%増、タブレット用OLED出荷は前期比54%増・前年比113%増となった。スマートフォン用OLEDとTV用OLEDは季節要因のため前期比で減少したが、前年比では2桁の伸びを示した。

「複数の用途で前年比プラス成長が続いている。市場が2022年と2023年上半期の悲惨な状況から2023年下半期に入って回復に転じ、成長が継続していることを示す喜ばしいニュースだ」とシニアディレクターのDavid Naranjoは述べている。

OLED出荷数および前年比成長率

Q1'24には、リジッド型OLEDスマートフォンが前期比25%増となったことで、スマートフォン用がOLED出荷数で84%のシェアを獲得、Q4'23のシェア79%から上昇した。OLEDスマートフォンでは、Huawei、Samsung、Oppoなど複数ブランドが前期比2桁成長を記録した。Samsungはリジッド型OLEDスマートフォンが前期比82%増、フレキシブル型OLEDスマートフォンが前期比32%増となり、全体では前期比56%増となった。

Quarterly OLED Shipment Report 速報版では、2016年以降Q1'24までの出荷実績データを、用途、ブランド、FPDメーカー、OLEDタイプなどの項目別に提供している。

出典調査レポート Quarterly OLED Shipment Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] OLED Panel Shipments Increased 50% Y/Y in Q1’24 on Y/Y Growth for Smartphones, TVs, Smartwatches and IT Applications

- In Q1’24, OLED units had 50% Y/Y growth, led by growth for monitors and tablets.

- In Q1’24, OLED smartphones and OLED TVs had Q/Q seasonal declines and Y/Y growth.

- In Q1’24, for OLED smartphones, several brands had double-digit Q/Q growth.

As revealed in DSCC’s latest release of the Quarterly OLED Shipment Report – Flash Edition, OLED panel shipments decreased 20% Q/Q and increased 50% Y/Y in Q1’24 after increasing 41% Q/Q and 31% Y/Y in Q4’23. In Q1’24, by select OLED applications, OLED monitor panel shipments increased 35% Q/Q and 189% Y/Y and OLED tablet panel shipments increased 54% Q/Q and 113% Y/Y. OLED smartphones and OLED TVs had seasonal Q/Q declines, but had double-digit Y/Y growth.

“The continued Y/Y growth for several applications is welcome news that the 2H’23 lift has continued to help the market to recover from a dismal 2022 and a first half of 2023," notes David Naranjo, Sr. Director.

In Q1’24, smartphones remained the largest OLED application with an 84% unit share, up from 79% in Q4’23 as a result of 25% Q/Q growth for rigid OLED smartphones. For OLED smartphones, several brands had double-digit Q/Q increases with Huawei, Samsung and Oppo leading the growth. Samsung had 56% Q/Q growth led by 82% Q/Q growth for rigid OLED smartphones and 32% Q/Q growth for flexible OLED smartphones.

The Quarterly OLED Shipment Report – Flash Edition, includes historical panel shipments from 2016 through Q1’24 by application, by brand, by panel supplier, by OLED type and much more.