OLED需給予測~供給過剰は緩やかに減少、しかし不足の兆候は見えず

出典調査レポート Quarterly OLED Supply/Demand and Capital Spending Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらDSCC Japan発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

記事のポイント

- モバイルおよびIT用途向けOLEDの供給過剰は2024年も続くが、2028年にかけて徐々に減少する。

- OLED供給で最も急成長しているのは、リジッドガラス基板に薄膜封止を施したもの (リジッド+TFE) である。

- TV用OLEDは、生産能力増強がないにもかかわらず2028年まで供給過剰が続く。

DSCCが Quarterly OLED Supply/Demand and Capital Spending Report 最新版 (Q2'24版) を発行、業界生産能力とOLED需要の最新予測を発表した。DSCCは現在、モバイルおよびIT用途のOLED需要の伸びが供給の伸びを上回り、過剰供給は5年間の予測期間を通じて徐々に減少すると予測している。

TV用OLEDについては、稼働率は徐々に改善していくが、2028年までの予測期間中はTV用OLEDが供給制約を受けることはない、とDSCCは見ている。

フレキシブルOLED (フォルダブル型およびローラブル型デバイス向けを含む) については、Samsungの生産能力シェアが予測期間を通じて下がる見通しで、中国系パネルメーカーの積極的な生産能力増強の影響により、同社のシェアは2021年の40%から2028年には31%に低下する。第2位はBOEで2028年には生産能力シェアを25%まで拡大、一方でLGDは2026年にTianmaに追い抜かれて第4位に転落すると見られる。

より大きなカテゴリーであるモバイルおよびIT用途向けでは、生産能力が最も急速に伸びているのは薄膜封止 (TFE) を施したリジッドガラス基板を使用するもので、一般にIT用途向けとなっている。Samsungはリジッド+TFEで最大の生産能力を有しており今後もトップサプライヤーであり続けるが、LGD、BOE、Visionox、Japan Displayもこのセグメントで競合すると予測される。

面積ベースのOLED需要は2022年に初めて減少し、2023年にはさらに減少した。これは、TV以外の用途の増加がTVの需要不振と在庫調整を克服するには不十分だったためである。DSCCでは、2024年からOLED TVが回復し再び成長すると予測しているが、OLED全体の面積需要に占めるTVのシェアは回復せず、2028年にはOLED全体の面積に占めるTVのシェアはわずか39%となりそうだ。また、「その他すべて」の用途の面積需要はIT用途 (モニター、ノートPC、タブレット) がけん引し2028年には全体の21%に上昇、スマートフォンのシェアはOLED面積需要の40%に低下する。

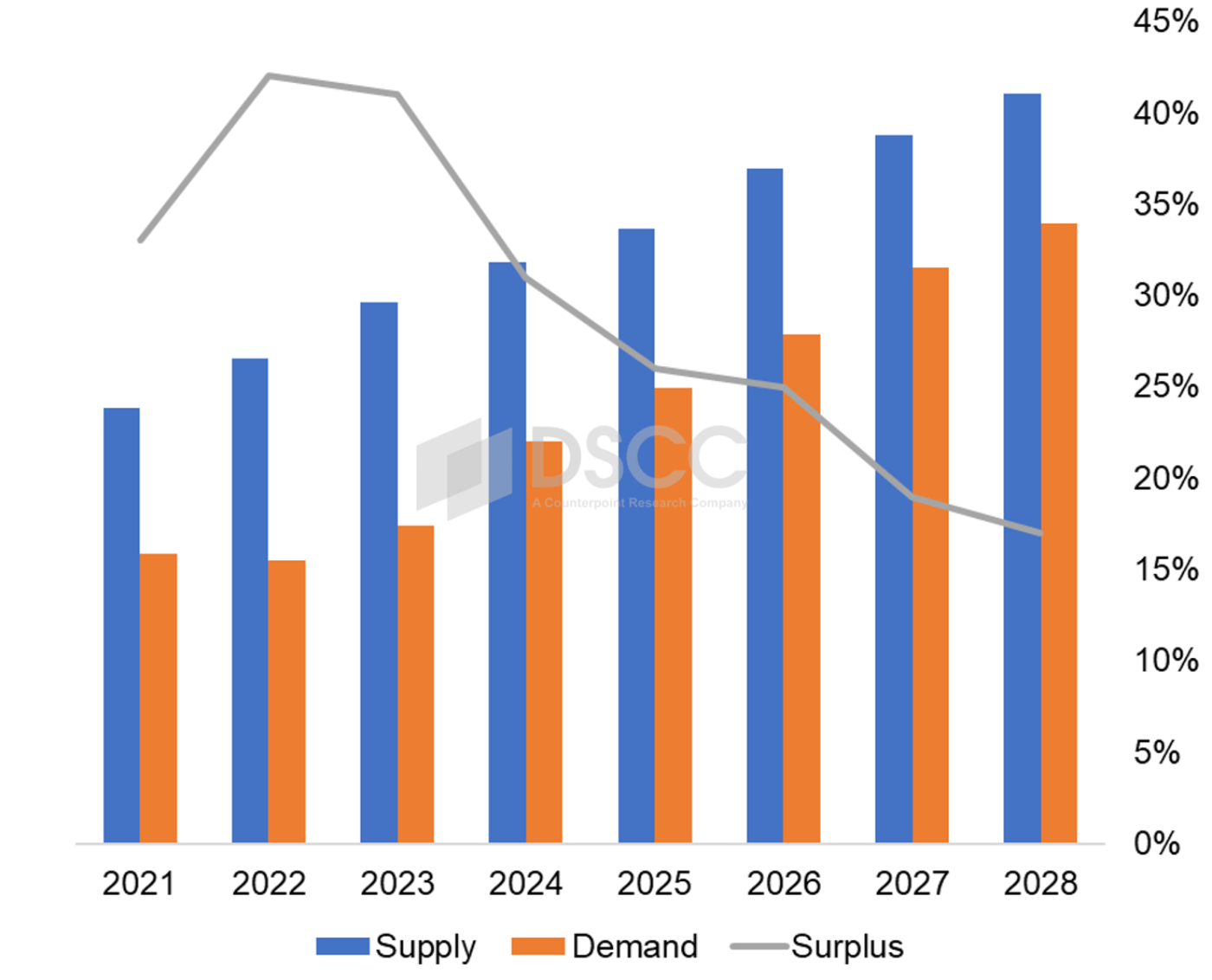

下図はDSCCのモバイルおよびIT用OLED需給予測である。2021年には需要の伸びが供給の伸びを上回ったため、モバイル用OLED全体の過剰生産能力は縮小したが、スマートフォン用リジッドOLEDの需要が急減したことで、2022年と2023年には過剰供給が拡大した。需要が着実に伸びる一方で供給の伸びは抑制されることから、2028年にかけて過剰供給は着実に減少するだろう。

モバイルおよびIT用OLED需給予測

大型用途では、2023年にTV/モニター用需要が2年連続で減少、前年比24%減と急落した。LGDとSDCの生産能力が増加した結果、余剰能力は2021年の9% (事実上の供給制約) から2023年には50%に膨れあがった。DSCCは予測期間を通じてTV用とモニター用のOLED需要増が供給増を上回ると見ているが、2028年には余剰が22%になると見られる。

出典調査レポート Quarterly OLED Supply/Demand and Capital Spending Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

[原文] OLED Supply/Demand – Oversupply to Slowly Decline but No Sign of Shortage

- Oversupply of OLED for mobile and IT applications persists in 2024 but will gradually decline to 2028.

- The fastest growing segment of OLED supply utilizes a rigid glass substrate with thin-firm encapsulation (Rigid+TFE).

- OLED TV will continue to be in oversupply through 2028 despite no capacity additions.

DSCC, a Counterpoint Research Company has updated its Quarterly OLED Supply/Demand and Capital Spending Report for Q2’24, with DSCC’s latest capacity outlook for the industry and the forecast for OLED panel demand. DSCC now sees demand growth for OLED for mobile and IT applications exceeding supply growth, and oversupply gradually declining throughout the five-year forecast period.

For OLED TV panels, while DSCC expects utilization to improve gradually, it does not expect that OLED TV panels will be constrained by supply through the duration of the forecast period to 2028.

In flexible OLED panels (which include panels for foldable and rollable devices), Samsung’s leading share of capacity will decline throughout the forecast as Chinese panel makers continue to aggressively add capacity, declining from 40% in 2021 to 31% in 2028. BOE is the #2 supplier by capacity and will grow its share of capacity to 25% by 2028, while LGD will be passed by Tianma in 2026 to fall to the #4 position.

Within the larger category of OLED for mobile and IT applications, the fastest growing portion of capacity utilizes a rigid glass substrate with thin-film encapsulation (TFE) and is generally directed at IT applications. Samsung has the largest capacity for Rigid+TFE and will remain the largest supplier, but LGD, BOE, Visionox and Japan Display are also expected to compete in this segment.

OLED demand area declined in 2022 for the first time ever and then declined further in 2023, as the increase in other applications was insufficient to overcome the soft demand and the inventory correction in TVs. Although DSCC expects that OLED TVs will recover starting in 2024 and will resume growth, TV’s share of overall OLED demand area will not recover, and by 2028 TV will be only 39% of all OLED area. The area demand for “all other” applications will climb to 21% of the total by 2028, driven by IT applications (monitors, notebooks and tablets), while smartphones fall to 40% of OLED area demand.

The chart below shows DSCC’s outlook for OLED panels for mobile & IT applications. While overall mobile OLED overcapacity was reduced in 2021 with demand growth outpacing supply growth, the sharp decrease in demand for rigid OLED panels for smartphones resulted in increased oversupply in 2022 and 2023. Steady growth in demand combined with more restrained growth in supply will reduce the oversupply steadily through 2028.

On the larger screen side, TV/Monitor panel demand in 2023 declined for the second straight year with a precipitous 24% Y/Y drop. With increased capacity for both LGD and SDC, the result is that the capacity surplus has ballooned from 9% in 2021 (effectively, supply constrained) to 50% in 2023. While DSCC expects that demand growth for OLED TV and monitor panels will exceed supply growth throughout the forecast period, the surplus is expected to be 22% in 2028.

The Quarterly OLED Supply/Demand and Capital Spending Report gives a comprehensive perspective on the OLED industry.