Q4'24の世界TV市場、TCLとHisenseが急浮上~MiniLED搭載TVで攻勢

出典調査レポート Quarterly Global TV Shipment and Forecast Report の詳細仕様・販売価格・一部実データ付き商品サンプル・WEB無料ご試読は こちらから お問い合わせください。

これらCounterpoint Research FPD部門 (旧DSCC) 発の分析記事をいち早く無料配信するメールマガジンにぜひご登録ください。ご登録者様ならではの優先特典もご用意しています。【簡単ご登録は こちらから 】

Q4'24の世界TV市場、TCLとHisenseが急浮上~MiniLED搭載TVで攻勢

Q4'24の世界TV市場でTCLとHisenseがともに過去最高シェアを記録した。Counterpoint Researchが先週発刊した Global TV Shipment and Forecast Report で明らかにしている。両社は地元である中国市場の追い風を受け、先端技術TV市場でのシェア獲得を目指しMiniLED搭載の大型TVを積極的に販売した。

Counterpoint Researchの Global TV Shipment and Forecast Report ではTV出荷数データをブランド、ディスプレイ技術、サイズ、解像度などの項目別に提供しており、市場ダイナミクスの理解に役立つレポートとなっている。白色OLED、QD-OLED、MicroLED、MiniLED LCD、QD-LCD、Nano Cell LCD、8K TVなど、すべてのディスプレイ技術を対象としており、22ブランド、8地域の情報を収録している。レポートではトップダウンの企業レベル調査とボトムアップのモデルレベルデータ収集を組み合わせており、数十年にわたる業界経験を通じて開発されたCounterpoint Researchの独自モデルを用いている。Q4’24実績は先週発表済みで、最新予測は今月末までに発表予定である。本稿では最新四半期と2024年についてレビューする。

Q4’24の世界TV出荷数は前年比2%増の6100万台だった。世界TV出荷額は前年比6%増の300億ドルだった。2024年通年の世界TV出荷数は前年比2%増の2億3100万台、世界TV出荷額は前年比2%減の1040億ドルだった。

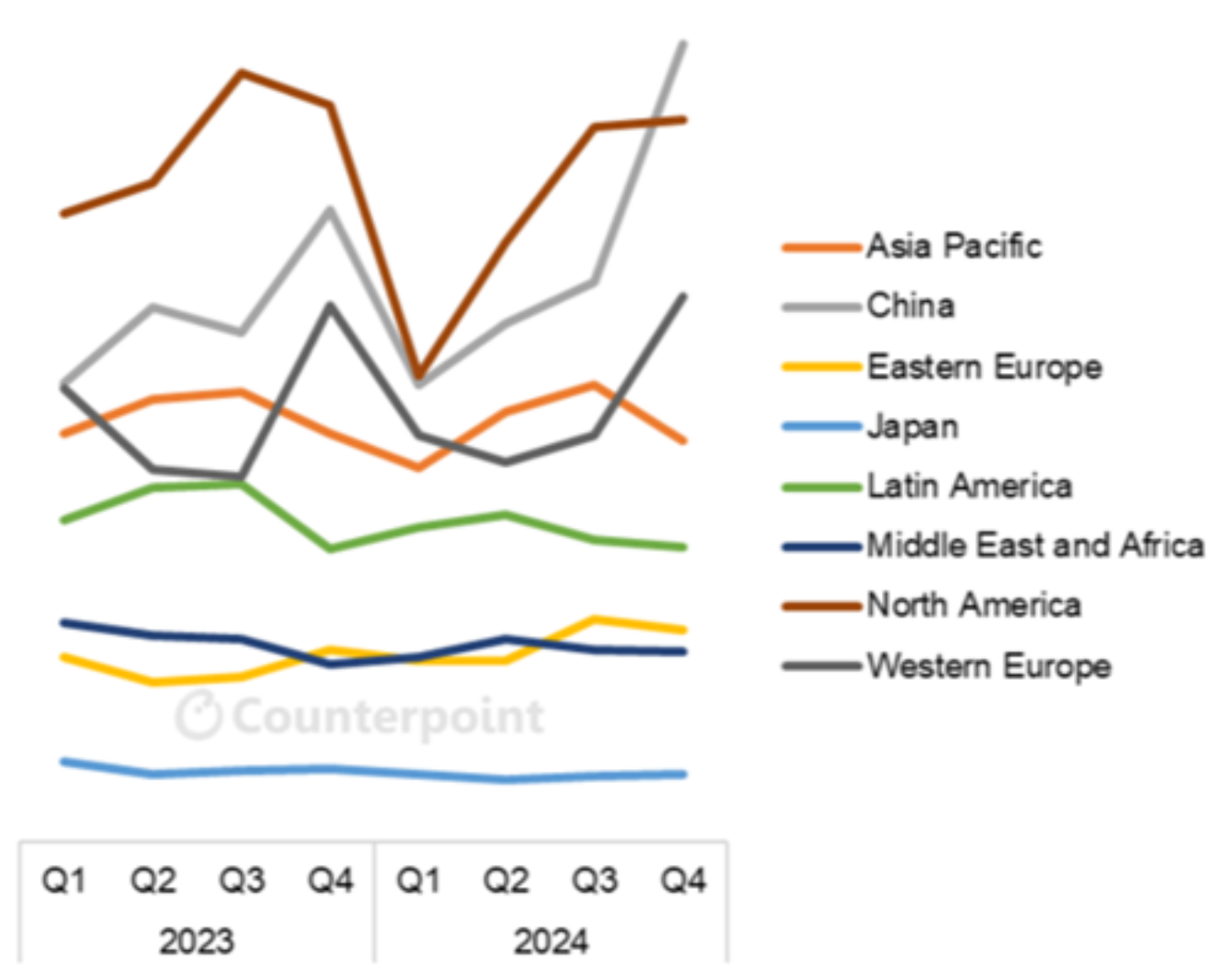

世界TV市場 地域別出荷額推移 (ドルベース)

一つ目のグラフは地域別出荷額推移を示している。北米と西欧は例年通り第4四半期に出荷額のピークを迎えたが前年比ではほとんど伸びず、西欧は前年比2%増、北米は前年比2%減となった。対照的に、中国のTV出荷額は前年比26%増と急増し、数年ぶりにTV出荷額ベースで最大の地域市場となった。

注目すべきは、出荷数がわずか1%増だったのに出荷額がこれほど伸びた点で、中国の消費者がより大型で高価なTVを購入したことがその要因である。このパターンは、より高価なTVに多額の補助金を支給する政府の補助金制度に助けられた。

中国市場の出荷額増加に加え、他の主要地域市場でのシェア拡大により、世界市場におけるTCLとHisenseのシェアが拡大することになった。TCLの出荷額シェアはQ4’23の11%からQ4’24には14%に、Hisenseの出荷額シェアはQ4’23の10%からQ4’24には13%に上昇した。

両社の成長は韓国大手2社の犠牲の上に成り立っている。世界のTV出荷額に占めるSamsungのシェアはQ4’23の28%からQ4’24には24%に、LGのシェアはQ4’23の16%からQ4’24には15%に低下した。

世界のTV市場における中国ブランドの躍進を支えた重要トレンドの一つは、超大型サイズTVの増加である。Q4’24の世界市場の前年比2%成長は大型サイズによるものだった。70インチ未満のTVは依然としてTV全体の86%を占めているが、出荷数は前年比1%減、出荷額は4%減だった。出荷数成長率は70-79インチが前年比8%増、80-89インチが前年比56%増、90インチ以上が前年比118%増で、サイズが大きいほど高くなっている。

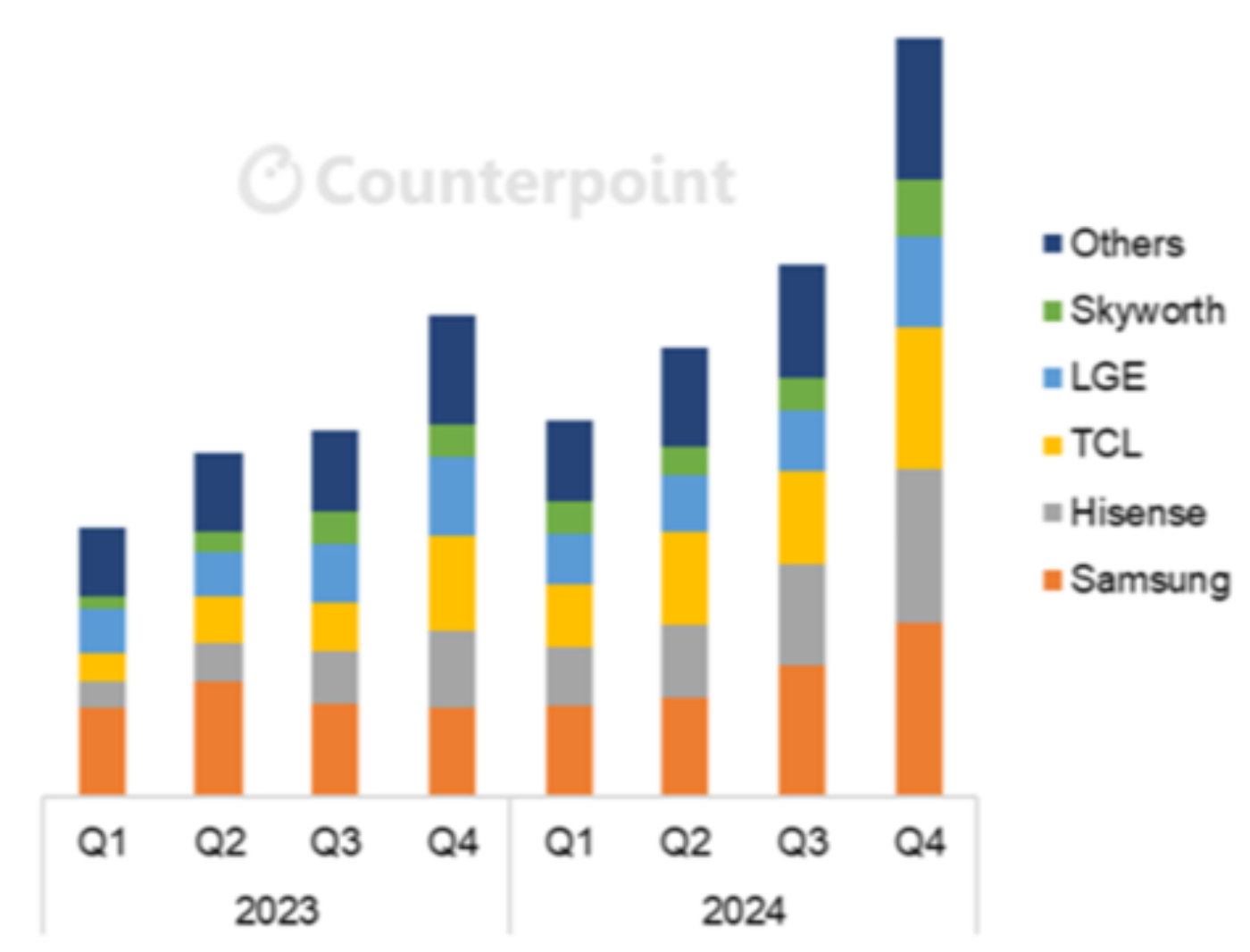

世界TV市場 ブランド別出荷数推移 (画面サイズ75インチ超)

この大型カテゴリーでは、Hisenseが前年比102%増の成長率で第2位に躍り出た一方、TCLが前年比48%増で第3位に転落した。LGEは前年比16%増にとどまり、超大型サイズでは大差の第4位となった。

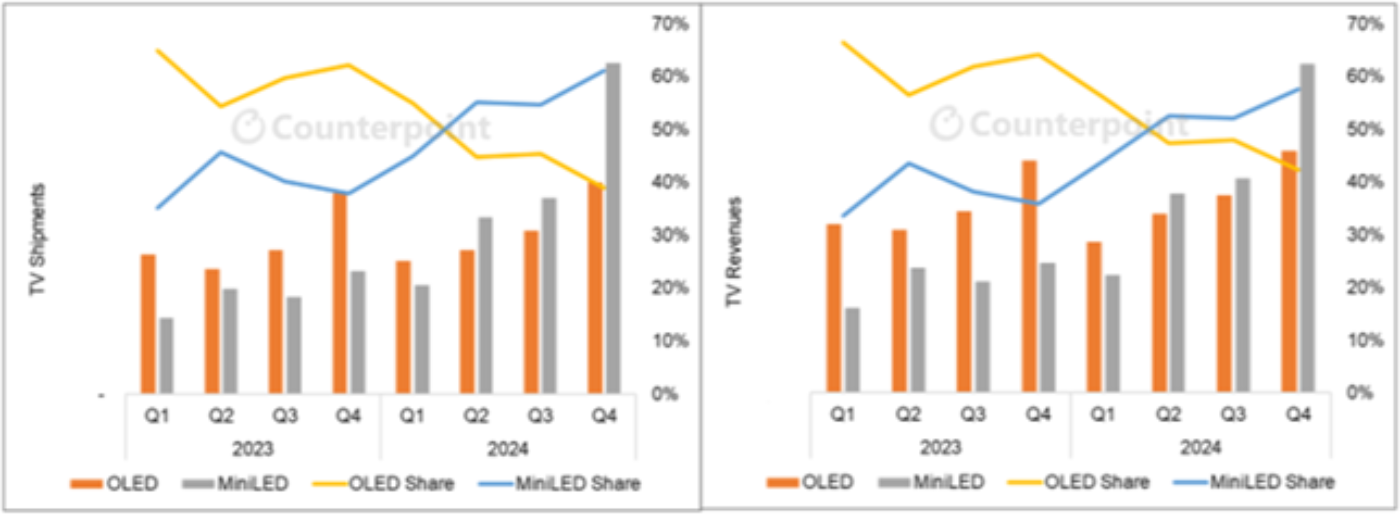

大型化トレンドと中国TVメーカーのシェア拡大に加え、MiniLED TVモデルの成長がTV市場の第3の主要トレンドとなっている。MiniLED TVはおもにOLED TVと同じような価格帯で競争しているが、TV 用ではOLEDとLCDのパネルコスト差があるため、消費者は小型のOLED TVか大型のMiniLED TVかの選択を迫られる。以下の2つのグラフが示すように、MiniLEDを選択する消費者が増えている。

OLED TVとMiniLED TVの出荷推移 (左:数量 / 右:金額)

Q4’24のMiniLED TV出荷数は前年比170%増、平均価格が1368ドルから1284ドルに低下したため、出荷額は前年比153%増となった。一方、OLED TVの出荷数は前年比5%増にとどまり、価格は1493ドルから1478ドルへとわずかながら低下したことから、出荷額は前年比4%増となった。「スーパープレミアム」セグメントにおけるMiniLEDのシェアは、数量ベースで61%、金額ベースで58%と過去最高を記録した。Q4’24のOLED TVの平均画面サイズは65インチだったが、MiniLEDの平均画面サイズは72インチだった。

Global TV Shipment and Forecast Report ではピボットテーブルの活用により、技術、ブランド、製品ライン、地域を横断した分析を実現している。レポートから得られるインサイトをいくつかご紹介しよう。

- 北米ではTCLのTV出荷数シェアが Q4’23の14%からQ4’24には16%に、Hisenseの出荷数シェアはQ4’23の11%からQ4’24には13%に上昇した。

- 世界で販売されるTVうち、36%が250ドル以下、67%が500ドル以下である。1000ドル以上で販売されているTVはわずか12%、2000ドル以上はわずか1%である。

- TVの82%は標準的LCD技術を採用しており、TV出荷額の61%を占めている。

- 先端TV技術を採用した18%のTVのうち半数がQD-LCDであり、MiniLED、白色OLED、Nano Cell、QD-OLEDの比率は低い。

- OLED TV市場ではLGDが出荷数、出荷額ともに50%以上のシェアを占め、依然優勢である。SamsungはSonyやPanasonicなどからシェアを奪い、Sonyを抜いてOLED TVのNo. 2ブランドとなった。

- かつてはMiniLEDの支配的ブランドだったSamsungだが、Q4’24のMiniLED出荷数ではHisense、TCL、Xiaomiに次ぐ第4位に転落した。

- Q4’24の中国におけるTV出荷数上位3ブランドは上から、Hisense、Xiaomi、TCLだった。出荷額でも上位3ブランドは同じ顔ぶれでHisenseがやはり首位、TCLがXiaomiを上回った。

[原文] TCL, Hisense Surge in TV Market in Q4 2024 With MiniLED Storm

TCL and Hisense both reached all-time highs in global TV market share in Q4 2024, according to Counterpoint Research’s Global TV Shipment and Forecast Report, released last week. The two companies rode tailwinds in their home market of China and aggressively promoted large MiniLED TVs to gain share in the premium TV market.

Counterpoint’s Global TV Shipment Report helps understand market dynamics by providing TV shipments by brand, display technology, size and resolution. The report covers 22 brands, 8 regions and all display technologies including White-OLED, QD-OLED, MicroLED, MiniLED LCD, QD-LCD, Nano Cell LCD and 8K TVs. The report combines top-down corporate-level surveys and bottom-up model-level data collection with Counterpoint’s proprietary models developed through decades of industry experience. Q4 2024 results were released last week, and an updated forecast will be released later this month. In this article, we will review the latest quarter and 2024.

In Q4 2024, global TV shipments increased 2% YoY to 61 million. Global TV revenues increased 6% YoY to $30 billion. For the full year 2024, global TV shipments increased by 2% to 231 million units while global TV revenues decreased 2% YoY to $104 billion.

The first chart here shows revenues by region. While North America and Western Europe saw the typical Q4 peak in revenues, there was little to no growth on a YoY basis, with Western Europe managing 2% growth YoY and North America declining 2% YoY. In contrast, TV revenues in China surged 26% YoY, making it the biggest regional market for TV revenue for the first time in years.

Remarkably, this revenue growth came from only a 1% YoY growth in units, as Chinese consumers purchased bigger, more expensive TV sets. This pattern was helped by a government subsidy scheme that provided a larger subsidy for more expensive TVs.

The revenue growth in the China market, plus market share gains in other key regional markets, drove global share growth for both TCL and Hisense. TCL’s revenue share increased from 11% in Q4 2023 to 14% in Q4 2024, while Hisense’s revenue share increased from 10% to 13% in the same period.

Those gains came largely at the expense of the two South Korean giants. Samsung’s share of global TV revenues fell from 28% in Q4 2023 to 24% in Q4 2024, while LG’s share fell from 16% to 15%.

Within the global TV market, one of the key trends that helped the Chinese brands make these gains was the increase in TVs with very large sizes. The global growth of 2% YoY in Q4 2024 came from larger sizes. For TVs under 70”, which continued to make up 86% of all TVs, unit volume decreased by 1% YoY and revenue decreased by 4%. Volume growth increased with increasing sizes – 70”-79” TV shipments grew 8% YoY, 80”-89” shipments grew 56% YoY and 90”+ shipments grew 118% YoY.

Within this larger-size category, Hisense jumped to second place in Q4 2024 with growth of 102% YoY while TCL fell to third place with 48% YoY growth. LGE fell to a distant fourth place in the ultra-large sizes on growth of only 16% YoY.

Coincident with the trend toward larger sizes and the share gains by Chinese TV makers, the growth of MiniLED TV models is the third major trend in the TV market. MiniLED TVs typically compete at price points similar to OLED TVs, but because of the cost difference between OLED and LCD TV panels, consumers face a choice between a smaller OLED TV or a larger MiniLED TV. An increasing number of consumers are choosing the MiniLED, as shown by the next two charts.

MiniLED TV shipments increased by 170% YoY in Q4 2024, and revenues increased by 153% as the average price decreased from $1,368 to $1,284. OLED TV shipments, meanwhile, increased by only 5% YoY and revenues increased by 4% YoY as prices edged down from $1,493 to $1,478. MiniLED’s share of the “super premium” segment increased to an all-time high of 61% in shipments and 58% in revenue. The average screen size of an OLED TV in Q4 2024 was 65”, while the MiniLED’s average screen size was 72”.

The pivot tables of the Global TV Shipment and Forecast Report allow for analysis across technologies, brands, product lines and geographies. Here are a few more insights from the report:

- In North America, TCL increased its share of TV shipments from 14% in Q4 2023 to 16% in Q4 2024 while Hisense increased its share from 11% to 13%.

- 36% of TVs sold globally go for less than $250, and 67% go for less than $500. Only 12% of TVs are sold for more than $1,000 and only 1% for more than $2,000.

- 82% of TVs employ standard LCD technology, and these generate 61% of TV revenues.

- Among the 18% of TVs employing a more advanced TV technology, half are QD-LCD, with MiniLED, White OLED, Nano Cell and QD-OLED having smaller stakes.

- LGD continues to dominate the OLED TV market with more than 50% share of both shipments and revenue. Samsung has displaced Sony as the #2 brand for OLED TVs, taking share from Sony, Panasonic and others.

- Samsung, once the dominant brand for MiniLED, fell to fourth place in MiniLED shipments in Q4 2024, behind Hisense, TCL and Xiaomi.

- Hisense, Xiaomi and TCL were the top three brands in terms of TV shipments in China in Q4 2024, in that order. In revenues, the top three were the same and Hisense also led, but TCL outsold Xiaomi.